What we cover

In November, we wrote about recent lows in sign prices — but ultimately, that movement in price wasn’t so unusual. While the national average price fell to a recent low under $3.00 per gallon, prices have dipped below that benchmark eight times since late 2023.

But then prices kept falling in December, and well, things are a bit more unusual now. Sign prices reached levels we haven’t seen in many years. And coupled with even steeper drops in rack prices, retailers benefitted from some of the largest margins in recent memory.

Read on for a recap of a remarkable month in fuel for drivers and business owners alike.

Last month’s data

Cheap oil, high supply, strong margins get even better

Let’s start with the foot traffic numbers in December, which were just about the only area where expected seasonal declines took hold. We generally expect colder weather and fewer commuters amid the holiday season to result in transaction drops, and that’s exactly what happened in 2025.

Fuel transactions were down about 3% month-over-month, while c-store transactions fell by a bit more. Those customers who did shop in-store, however, tended to spend more — and that made up for the reduction in visitors. Overall, c-stores actually made more money in December than they did in November, with stores in the Northeast improving the most nationally.

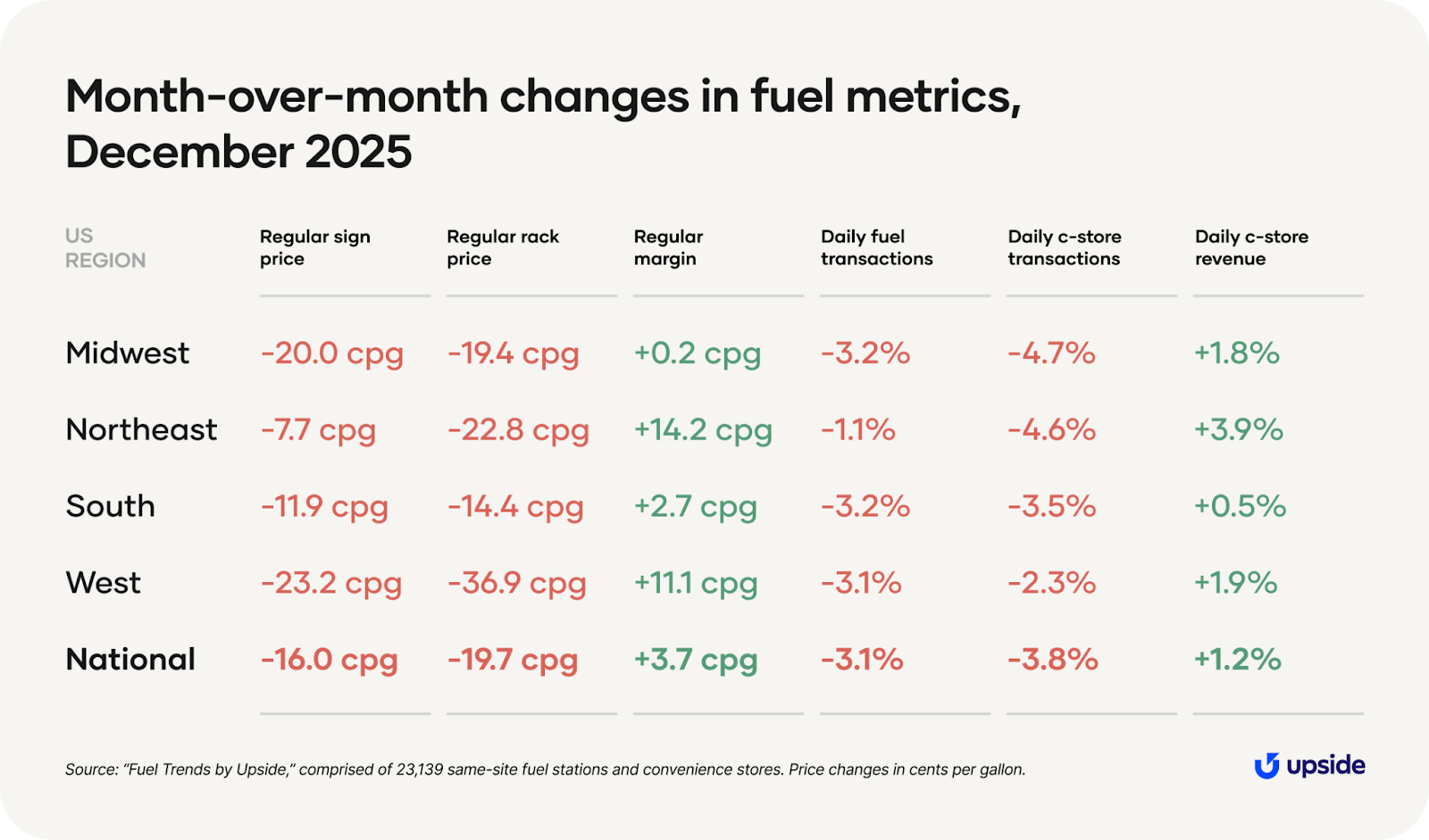

Now, let’s dig into prices, the headline metrics of the month. The average American gas station charged 16 cents per gallon less for regular fuel in December than they did in the previous month. Prices in each region fell considerably, but the largest drop occurred in the West, followed by the Midwest.

In addition to these meaningful declines in sign price, the industry also experienced lower rack prices in December. Stations in all regions saw double-digit declines in rack prices, with the average American station paying nearly 20 cents per gallon less than they did in November. The most notable decline here was once again in the West, as the region recovered from a minor supply disruption due to a refinery fire.

These lower rack prices are due to two variables in particular: cheaper oil and higher refinery supply. West Texas Intermediate (WTI) oil prices in December were just over $58 per barrel, the lowest level since January 2021. Furthermore, the US Energy Information Administration reported that due to increased supply abroad following fall maintenance, they expected lower crack spreads (a number representing refinery profit on each barrel of oil they produce).

Rack prices dropping more than sign prices? Sounds like a recipe for great margins — and that’s the focus of our recap this month.

Already-strong fuel margins reach recent highs

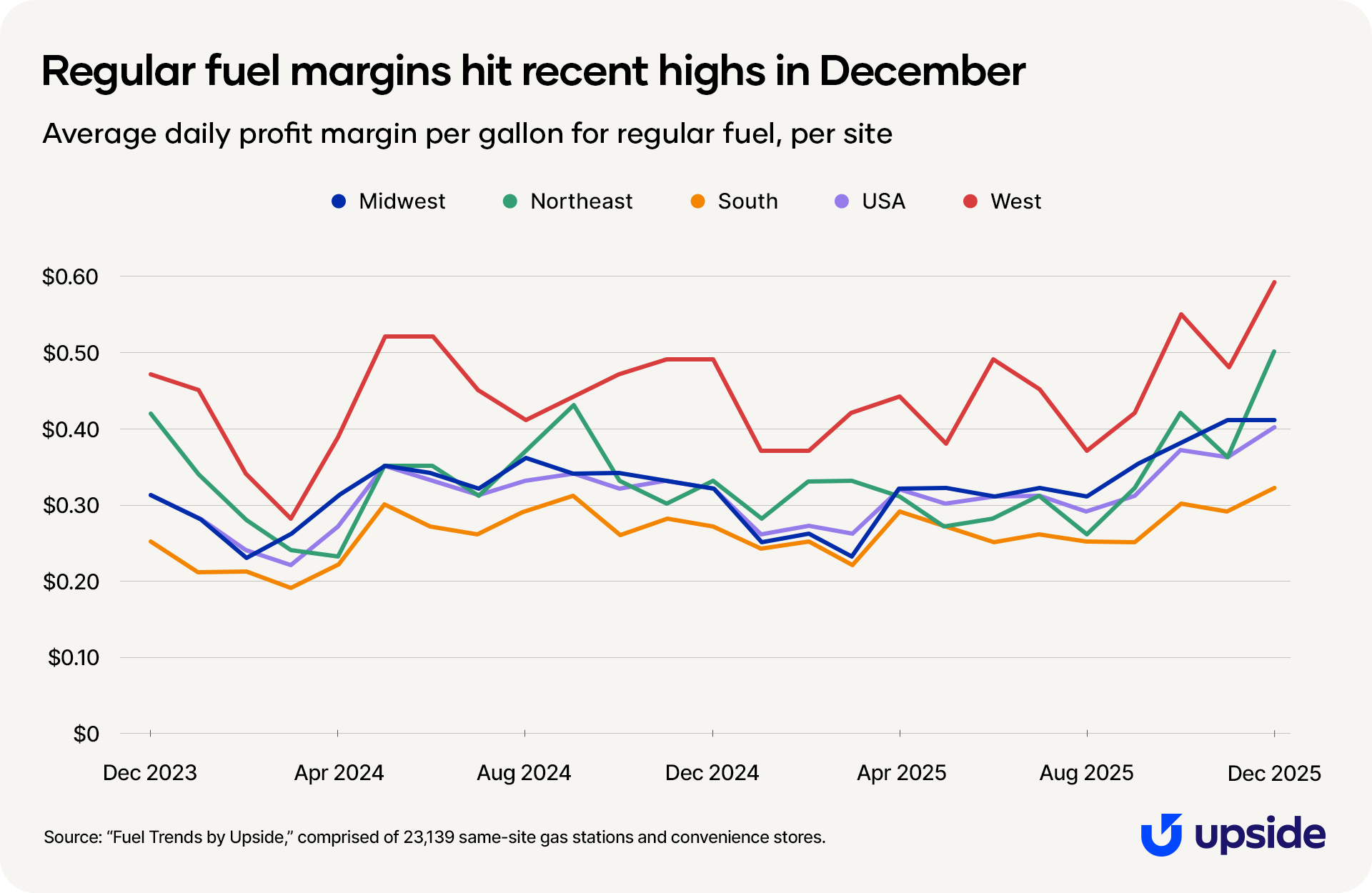

In December, regular grade margins increased for all regions — ultimately hitting their highest levels in the past two years. The average American station saw a modest increase of about 4 cents per gallon month-over-month, eclipsing 40 cents per gallon overall.

Month-over-month, the biggest boost came in the Northeast, where margins jumped more than 14 cents per gallon from November. The West, too, saw a considerable increase of 11 cents per gallon.

Meanwhile, the South and Midwest already had above-average margins for their regions, so in December they experienced more moderate increases.

The chart below shows how margins have changed over the past two years.

Why is it that margins differ across regions? Each region’s margin reflects the level of demand, competitiveness, and the cost of doing business in that particular area. Those factors can vary widely across the country.

The below chart shows recent profit margins for the typical gas station, broken down by division (specific subregions defined by the Census Bureau).

Predictions and considerations

Are big margins here to stay? And what’s happening in Venezuela?

Will the good times last for fuel retailers? It’s the question on everybody’s minds. Margins are looking strong right now, but how long can we count on that being the case?

With supply high and rack prices low, things look optimistic in the short run. Lower rack prices can help maintain higher margins for retailers.

At the same time, though, fuel retailers face high competition between stations and weak consumer demand in the long run. If they try to cut sign prices to win more trips, that will put downward pressure on margins.

With those two factors working against each other, where will things end up? There might be some small fluctuations in margin as oil prices change in the coming months. Ultimately, we predict the national average will settle somewhere between 30 and 35 cents per gallon in 2026.

But if you’ve read our past updates, you know that we often say international conflict has the potential to upend the industry. And of course, many people are discussing the implications of the United States’ military action in Venezuela at the beginning of January. American forces carried out a raid that resulted in the capture and indictment of President Nicolás Maduro.

To date, the events in Venezuela have influenced news headlines more than they have fuel prices. Venezuela only contributes 0.8% of the global oil production. However, the country also possesses the world's largest untapped oil reserves. This means the short-run impact of the events in Venezuela will likely raise fuel prices slightly in the United States, but could lower prices more considerably in the long run (think up to 10 years from now) if Venezuelan production increases closer to its potential.

Potential tailwinds:

1. While one conflict ramps up, another has been inching towards an agreement. If Ukraine and Russia reach a resolution to end fighting, that could possibly increase global oil supply and reduce prices for consumers.

2. As highlighted above, sign prices are at recent lows. Drivers tend to buy more gas when sign prices are low.

Potential headwinds:

1. American military action in Venezuela could reduce supply — though not by much, since Venezuela only produces a small fraction of global oil.

2. January is typically the month we see seasonal travel hit its lowest point of the year. Foot traffic declines work against low prices and high margins, and visits won’t begin ticking up until the winter weather thaws.

3. The economy is displaying mixed signals, with performance unevenly distributed. Assets like stocks and real estate have been growing in value steadily, but economic indicators like the unemployment rate are weak. Lower-income consumers are more likely to feel pessimistic about the economy and report a pullback in their spending, a phenomenon we’re calling the “income divide.” Read more in Upside’s new Consumer Spend Report.

Want a closer look at the data?

Check out our insights hub with all our fuel and convenience monthly updates, plus special industry reports.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.

{kind=link}