What we cover

Consumer confidence is fracturing along income lines — and retailers need to respond accordingly.

In our inaugural 2024 Consumer Spend Report, we analyzed more than one billion transactions across four spend categories and heard from 7,000+ consumers. We learned that, despite positive economic indicators, shoppers remained skeptical about the strength of the American economy. As a result, nearly 60% said they planned to cut back their spending.

A year later, the economy has changed once again. Indicators point to a weak labor market, elevated prices, and rising inflation. Ongoing uncertainty around tariffs has reintroduced cost volatility into everyday spending categories, further muddying the picture.

How are shoppers reacting to these changes? Our research shows mixed results. On one hand, roughly half of consumers told us they think the economy is getting worse in 2025. That’s a smaller group than in 2024 — but with an important difference. Economic confidence isn’t evenly distributed. Higher-income households are significantly more likely to say that they are hopeful about both the economy and their own financial picture. Lower-income households, meanwhile, feel like they’re getting left behind.

This sentiment gap translates into spending trends. The lower-income group says they are cutting back on spending, while the higher-income group says they spent more, sometimes considerably more.

Let’s dive into the data to find out what’s going on with consumer economic sentiment — and what it could mean for retailers in 2026.

Economic pessimism eased only slightly in 2025.

In all, 49% of our consumer respondents said the economy was worse in 2025 than 2024.

Several factors are driving pessimism. For many, pandemic-era savings have run out. The labor market is still strong, but unemployment is ticking up. Nearly every metric used to determine the strength of the economy "is somewhere between moderately concerning" and "virtually stagnant," according to Ben Harris, vice president and director of Economic Studies at the Brookings Institution.

Surprisingly, our survey results show that consumer optimism is actually increasing year-over-year. Compared with 2024, 7% fewer consumers say the economy is worse now, and 11% more say it is better.

While sentiment is improving, there’s a great deal of nuance when you dig into the data. Not everyone feels more confident in the economy.

Economic optimism divides along income lines

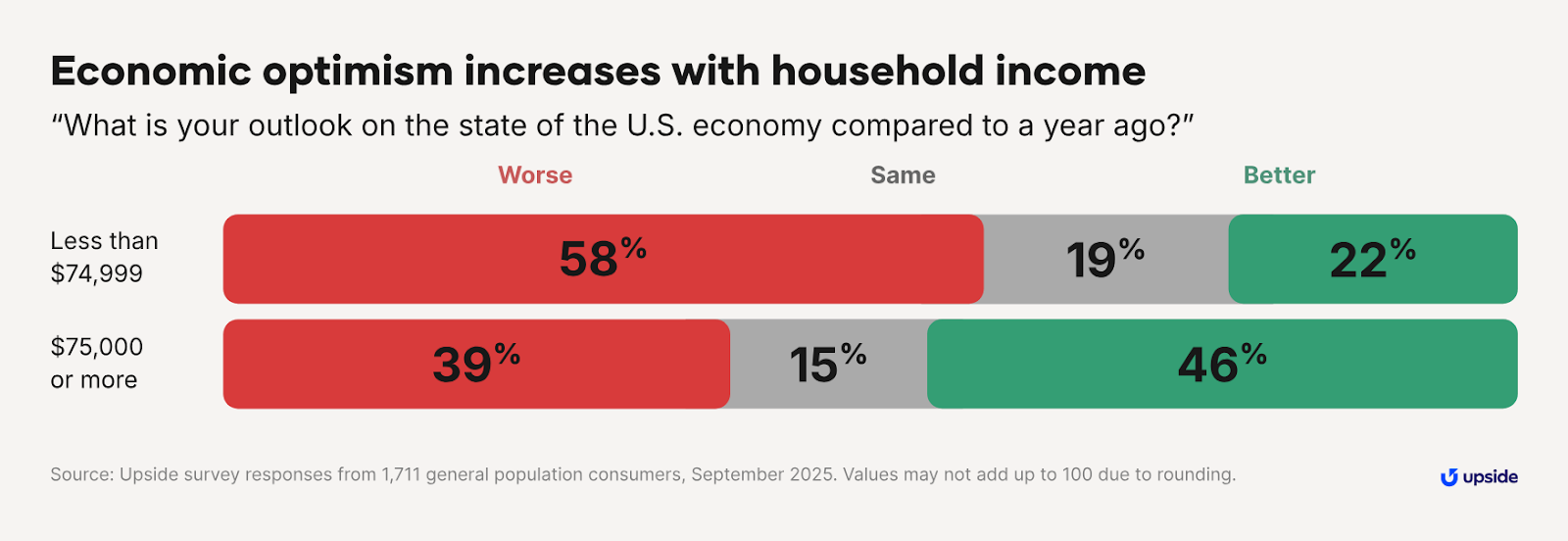

This year’s data showed that economic optimism increases with household income, creating an “income divide.” You might’ve also heard this referred to as a “K-shaped economy.”

In our survey, we see a widening gap in confidence, with the split occurring at an annual household income of $75,000.

Households above that income line feel better about the economy than those below it. More than 45% of high-income households feel better about the US economy compared to a year ago; only 22% of low-income households said the same.

This confidence has a direct impact on buying habits. When we asked our respondents to gauge how their spending levels changed year-over-year, the lower-income group reported cutting back. Higher-income consumers are willing to spend more to maintain or upgrade their lifestyles, offsetting some of the pullback among lower-income shoppers.

When you look at the data by retail category, there are more interesting trends. Lower-income shoppers are even cutting back on fuel and groceries, two non-discretionary spending categories for many Americans. They’re saving by simply driving less, combining errands into fewer trips, or using alternative forms of transportation. Some are making lifestyle changes, such as eating less meat, to save money.

“I try to spend less by using store brands and having smaller, less expensive meals,” said one woman in the 65+ age group and $25,000 – $49,999 income bracket.

Market pressures continue to weigh on consumer confidence

In 2025, tariffs led to higher prices for imported and domestic goods. Harvard’s research found that imported goods were 6.6% more expensive, while domestic goods cost almost 3.8% more.

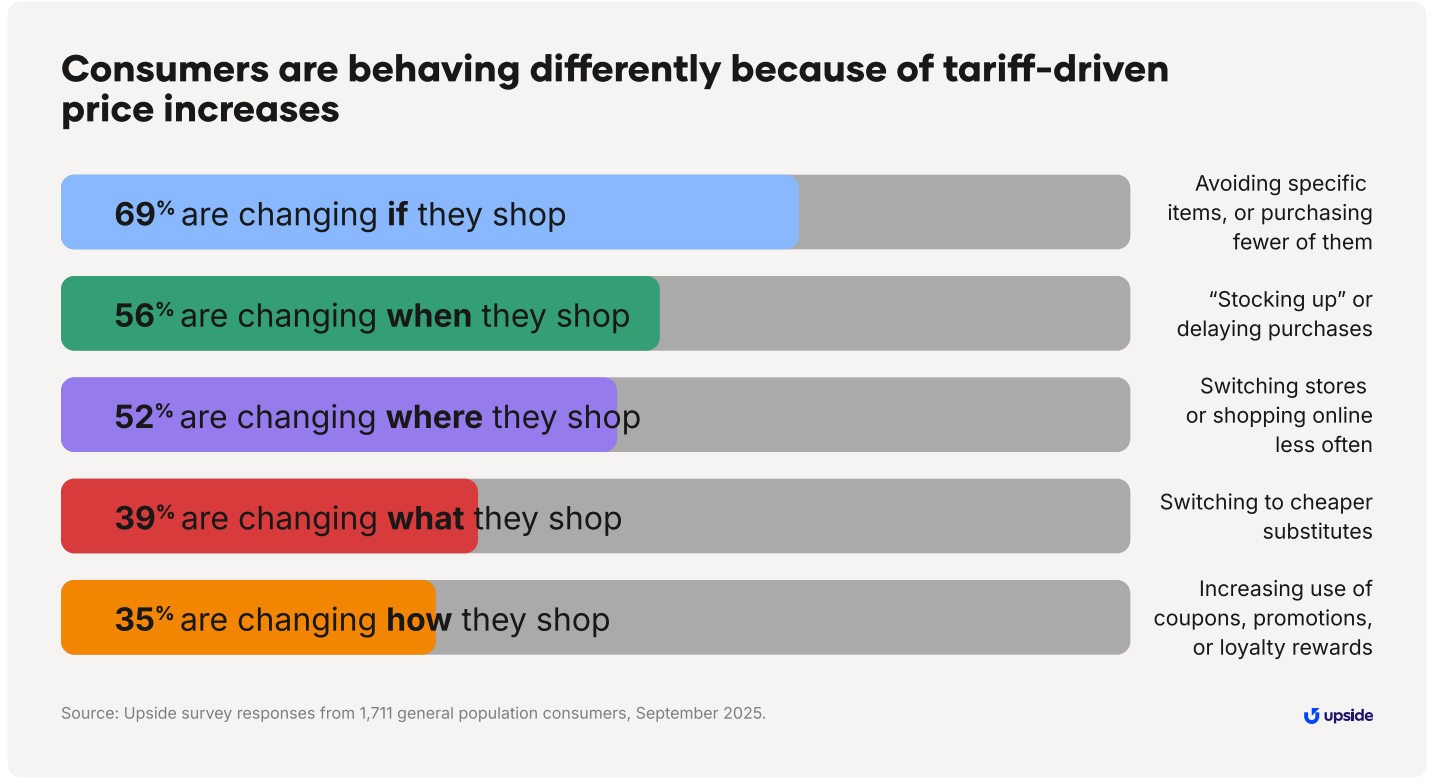

These price increases had a direct and reportable impact on shopper behavior. Our survey found that four in five consumers (79%) have changed their behavior due to tariffs. The ways consumers are adapting to tariffs vary widely, but the most common lever is cutting back spending.

Even higher-income customers are changing their shopping habits, spending selectively and being conscious about value. One Millennial female respondent with a household income in the low-six figures said her spending has decreased simply because she has “bought less stuff” than before.

Price sensitivity is one of the major forces driving shoppers. And, it’s not just tariffs that are causing consumers to feel the pinch. Persistent inflation and a soft labor market are also causing shoppers to delay spending or look for deals. Even small price increases can prompt customers to reconsider where they buy — or whether they buy at all.

Availability is another factor influencing how shoppers behave. The pandemic forced many businesses to operate online to stay available during lockdowns. As a result, it’s now easier than ever for shoppers to compare options and switch stores. For example, frequent online grocery shoppers buy from three times as many stores as their in-store-only counterparts.

And, with more options than ever before, the boundaries between different retail categories are shifting (or disappearing altogether). Convenience stores now offer fresh food, while grocery stores compete with grab-and-go meal options. More businesses are competing for a limited share of shoppers.

“I’ve compared prices more and I have gone to different stores to get the best deals on things that I need. Never had to do it before.” — Female, age group 65+ | $50,000 – $74,999 income bracket

Shoppers demonstrate more price checking, lower retailer loyalty

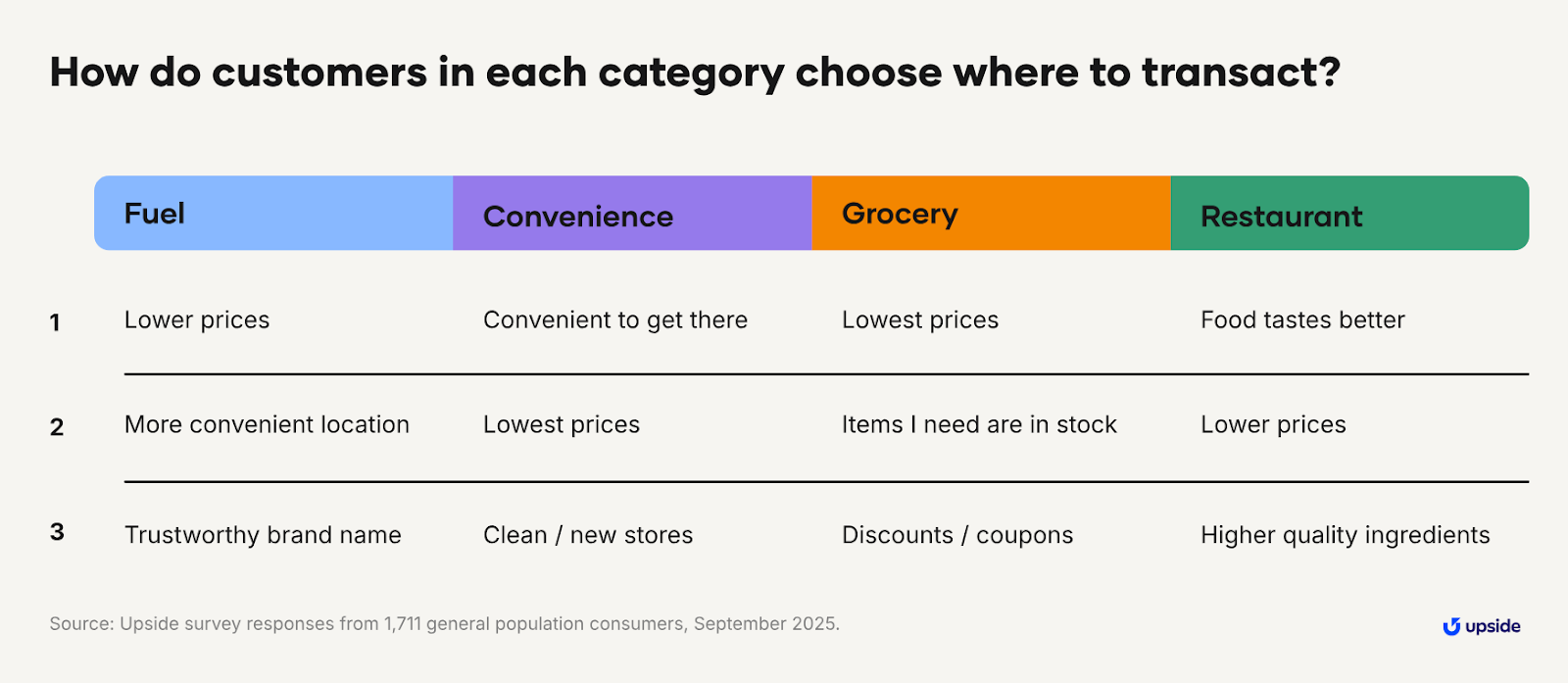

Value is the main driver for the uncommitted shopper, but it’s not the only factor determining where consumers transact. Purchase decisions are made one transaction at a time, with convenience, brand reputation, discounts, and other considerations impacting behavior. Here are the top criteria for each category:

Grocery customers are the most likely to compare prices across locations, with 60% reporting they shop around for the best deals. This is followed by 54% of fuel customers, 41% of convenience store customers, and 37% of restaurant customers. Across retail categories, the average US consumer has increased the number of locations they shop at. For instance, the average consumer now visits 3.1 grocery stores per month, up 8% year-over-year. Convenience stores saw the highest change, a 17% year-over-year increase at 3.2 stores per month.

Bottom line: sentiment isn’t abstract — it has real effects for retailers. This dynamic represents both a challenge and an opportunity. Retailers can push to win every transaction, even from new and lapsed customers.

Key takeaways for 2026

2025 was a year defined by economic and geopolitical uncertainty, income divergence, and shifting spending behaviors. This creates a challenging operating environment for retailers—and an opportunity. Those who understand and adapt to sentiment-driven behavior stand to win.

In 2026, retailers need to be equipped to win every next transaction. If customer loyalty is never assured, then flexibility and agility are mission-critical. Tailored promotions and personalized offers sent at the right time can have an outsized impact. “Offering the right product at the right price at the right time has become more important and harder to do than ever, especially as digital platforms enable consumers to comparison shop” (McKinsey).

Retailers should target premium products and enhanced services to higher-income consumers, who continue spending but with greater price sensitivity. For lower-income segments, formal loyalty programs and consistent discounts prove particularly effective at preventing store switching. Meanwhile, digital tools that simplify deal redemption appeal broadly across all consumer groups.

To learn more about the consumer economic sentiment and how to adapt your strategy, download The Consumer Spend Report 2025 for full data, vertical breakdowns, and deeper insights.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.