What we cover

Lingering economic pressures from 2025, plus an uncertain start to 2026, are shaping how consumers make hard choices about how every dollar is spent.

Our second annual Consumer Spend Report sourced insights from 10+ billion retail transactions at 21,000+ retailers, along with 11,000+ consumer and retailer survey responses, to understand why shoppers make the choices they do. It revealed how consumers are navigating lingering price fatigue, inflation, tariff uncertainty, a “soft” employment market, and income divergence.

As market uncertainty forces Americans to rethink where, when, and how they spend, the retailers who decode these new priorities — and adapt fastest — will win in 2026.

Get your copy of the Consumer Spend Report

Consumers are prioritizing value across every income level

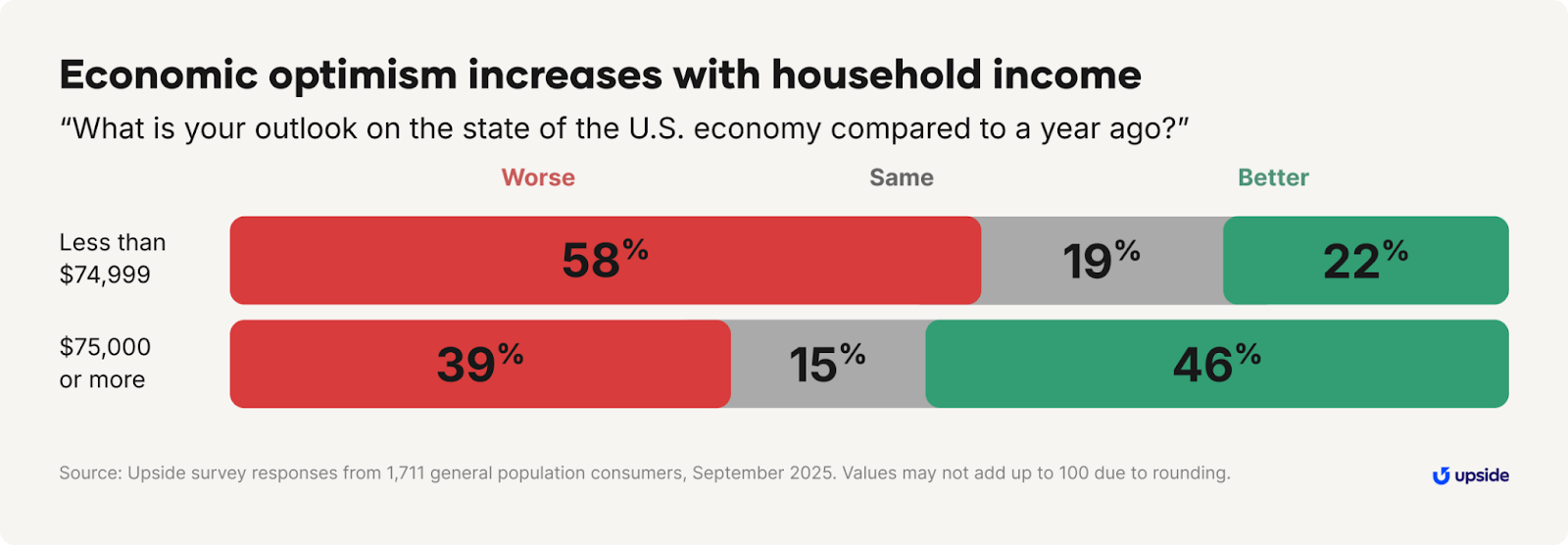

Roughly half of the consumers we polled (49%) told us they think the economy is getting worse. On one hand, pandemic-era savings have run out. On the other hand, tariffs and inflation have increased prices across the board. Imported goods were 6.6% more expensive, while domestic goods cost almost 3.8% more.

Digging deeper into the data reveals some surprising nuances. Economic pessimism isn’t evenly distributed. Households earning at least $75,000 per year are more likely to feel hopeful about the economy and their own financial picture. Those below that threshold feel like they are being left behind.

How does this “income divide” translate into spending behavior? When we asked survey respondents to estimate how their spending levels changed in the last year, the lower-income group reported cutting back, while the higher-income group said they spent more, sometimes considerably more. You might’ve also heard this phenomenon referred to as a “k-shaped economy.”

Given that this is a self-reported perception, it’s difficult to determine whether higher-income consumers actually spent more. But at the very least, high-income households appear willing to spend more, while lower-income consumers report cutting back in every category — even fuel and grocery, two types of purchases that are non-discretionary for many Americans.

Regardless of income, the main driver for all consumers in this economy is value. We see all kinds of customers exhibiting uncommitted behavior, shopping across different locations and formats to prioritize their own needs over brand loyalty.

Fragmented spending is now the norm

In all retail categories, consumers are visiting more sites and making more trips with smaller transaction totals — a sign of growing fragmentation in their shopping behavior. It’s easier than ever to split spending across multiple stores.

The growth of online retail has made it easier than ever to compare prices with just a few swipes on a smartphone. Frequent online grocery shoppers, for instance, buy from three times as many stores as their in-store-only counterparts. Competition has increased between retail categories, too. Convenience stores now offer fresh food, while grocery stores are adding grab-and-go meal options.

In 2025, the average US consumer in each category transacts at:

- 3.1 grocery stores per month (+8% YoY)

- 2.6 gas stations per month (+7% YoY)

- 3.2 convenience stores per month (+17% YoY)

- 4.0 restaurants per month (+3% YoY)

This data captures how consumers spread their spending across multiple retailers — splitting baskets, deal-hunting, and switching brands trip by trip.

“I've started buying more in bulk and using cash-back apps to save on everyday purchases. Also, I'm being more mindful about dining out, choosing more affordable spots.” — Male, age group 18-24 | $150,000+ household income

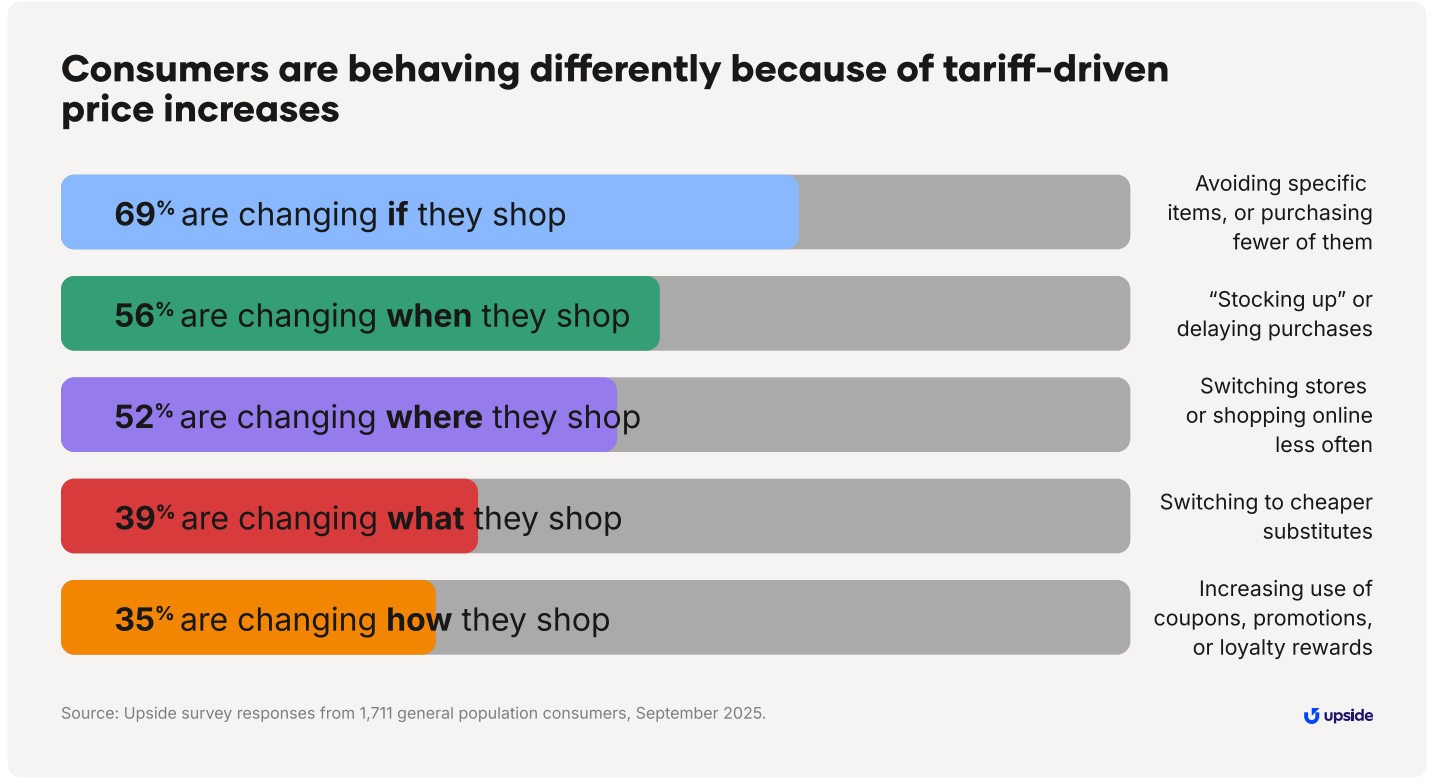

Tariffs are influencing what, when, and where consumers buy

Amid the many mixed economic signals, tariffs have emerged as one of the biggest drivers behind adaptive value-seeking. In 2025, four in five consumers (79%) said they have changed their behavior because of tariff-driven price increases. The primary response to tariffs has been to cut back on spending, but there are other ways consumers are changing their patterns.

Even higher-income households say they’re adjusting their behavior in response to tariff pressure. One Millennial man with a household income in the low-six figures said he’s “cut back on dining and switched to generic brands” in response to inflation and tariff-related pressures.

For retailers, understanding that tariff pressure is the major catalyst behind uncommitted shopping represents both a challenge and an opportunity. Retailers can push to win every transaction, even from new and lapsed customers.

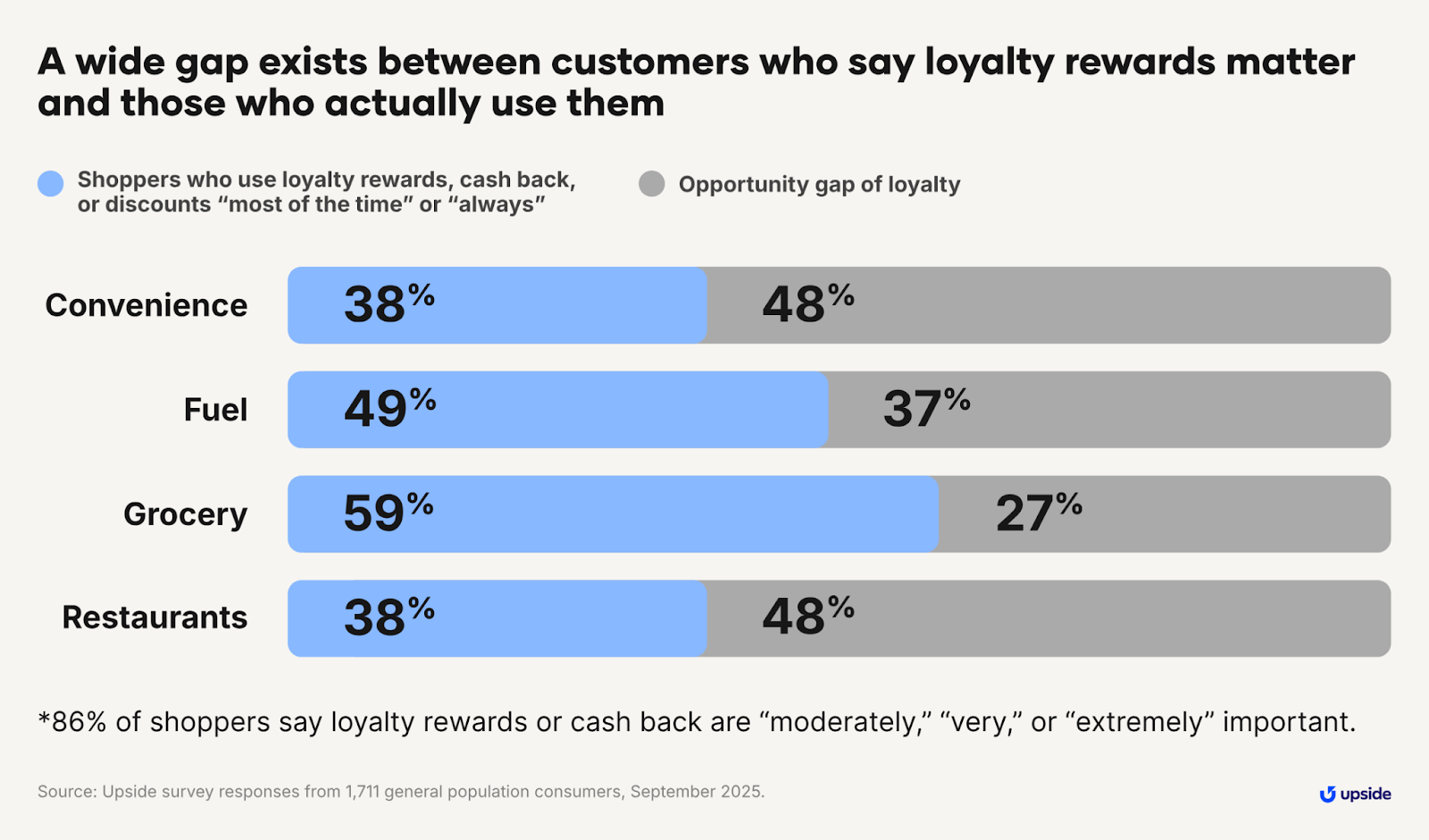

Loyalty programs are important to customers, but consistent usage remains low

The data we’ve highlighted can make customer retention feel daunting. Brand loyalty isn’t what it used to be; retailers now have to consider how to win every next transaction. So, what does this mean for loyalty programs?

First, loyalty programs still offer value to shoppers. Eight in 10 consumers say they find rewards or cash back important.

Although consumers see the value in loyalty programs, it doesn’t always translate into consistent usage. Our survey shows that only a minority of consumers actually use loyalty programs consistently. Retailers, too, report that loyalty participation and loyal behavior are flat, despite rising investment.

What we’re seeing is a gap between action and intent. Although customers want loyalty programs, very few use them frequently.

Loyalty programs still have relevance, though. Surprisingly, higher-income consumers are more likely to use loyalty programs than lower-income shoppers. They are also more willing than lower-income customers to change stores due to these programs.

This dynamic is telling us that shoppers want value, but lack incentives strong enough to shape store-choice habits.

Uncommitted behavior is here to stay — and retailers must adapt

Tariffs, cost fatigue, and income divergence put pressure on shoppers in 2025, encouraging value-seeking shopping choices and reinforcing market fragmentation. As we enter 2026, we are seeing consumers demonstrate behavior that is less predictable, more selective, and less brand-loyal.

Uncommitted behavior is here to stay, and retailers who understand these pressures will be able to design strategies — like personalized promotions — that resonate.

Explore the full data set in Upside’s 2025 Consumer Spend Report.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.