What we cover

We’ve previously analyzed how major weather events can increase fuel demand. For example, 2024’s Hurricane Helene caused a dramatic spike in gasoline sales in Florida and North Carolina.

However, January data shows how a natural hazard like an arctic cold wave can do the opposite. Winter Storm Fern barreled through America in mid-January, dumping heavy snow or dangerous ice on more than a dozen states.

Take a look at how weather and other factors shaped the month in fuel right here.

Last month’s data

Sanctions stunt supply, while a storm hampers demand

At the end of 2025, oil prices hit recent lows. Once the calendar turned to 2026, though, prices started to creep up — West Texas Intermediate oil reached $80 per barrel in January.

We can point to a few different factors that caused this. First, stronger sanctions on Russian and Iranian oil tightened the global supply. And secondly, we saw higher energy demand in North America due to extreme winter weather. (More to come on that.)

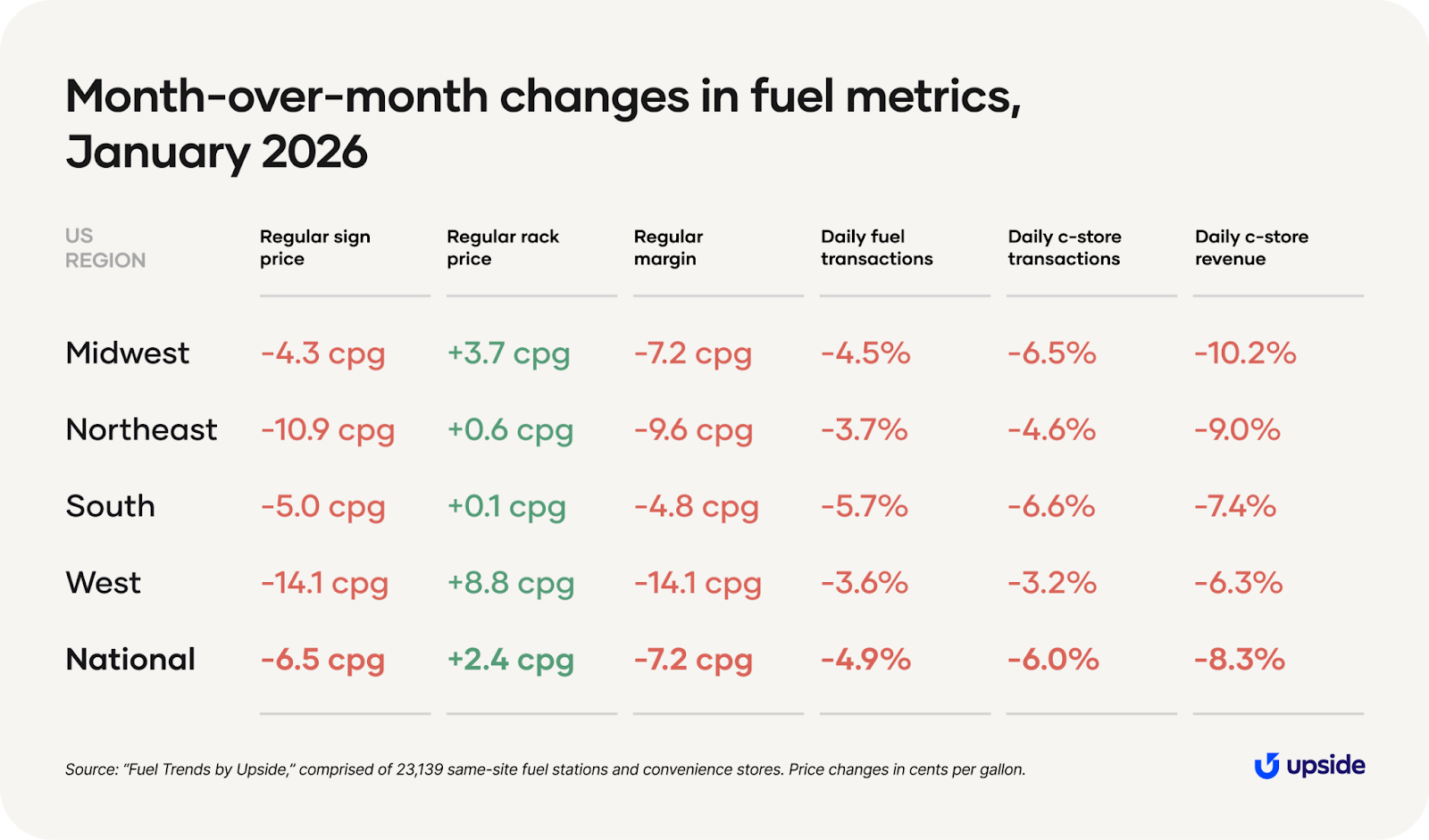

Overall, coming off a dramatic drop, January delivered a modest 2.4-cent increase in the national average rack price for a regular gallon of gas. The West experienced the largest uptick, with a more modest increase in the Midwest followed by negligible ones elsewhere.

That change has not yet passed on to sign prices, which actually decreased month-over-month. Out West, sign prices dropped more than 14 cents per gallon per station for regular. Oregon stations led the way in the region with a 25-cent drop, possibly due to the fact that the state was recovering from a pipeline disruption at the end of 2025.

Taken together, the typical American station saw a drop of 7 cents per gallon in regular margin month-over-month. We asked the question last time, and we received a quick answer — indeed, those high margins from December were not sustainable.

These trends are not too surprising. Coming off a month with declining rack prices and increasing margins, stations decided to give up margin to attract more customers in January. We'll keep an eye on this for next month, with a lot of unknowns on the supply side but an expected increase in sign prices.

And on that note, pencil in January 11, 2026, as the low point for sign prices this calendar year. That day, regular sign prices dipped to $2.75 per gallon, slowly rising for the remainder of the month. As the weather continues to warm and more drivers hit the roads in the coming months, we don’t expect sign prices to fall again until next winter.

On the demand side, most retail sectors see a decline in spending in the first month of the year — we switch from the holiday celebrations of December to the wellness resolutions of January. Fuel and convenience are no exception.

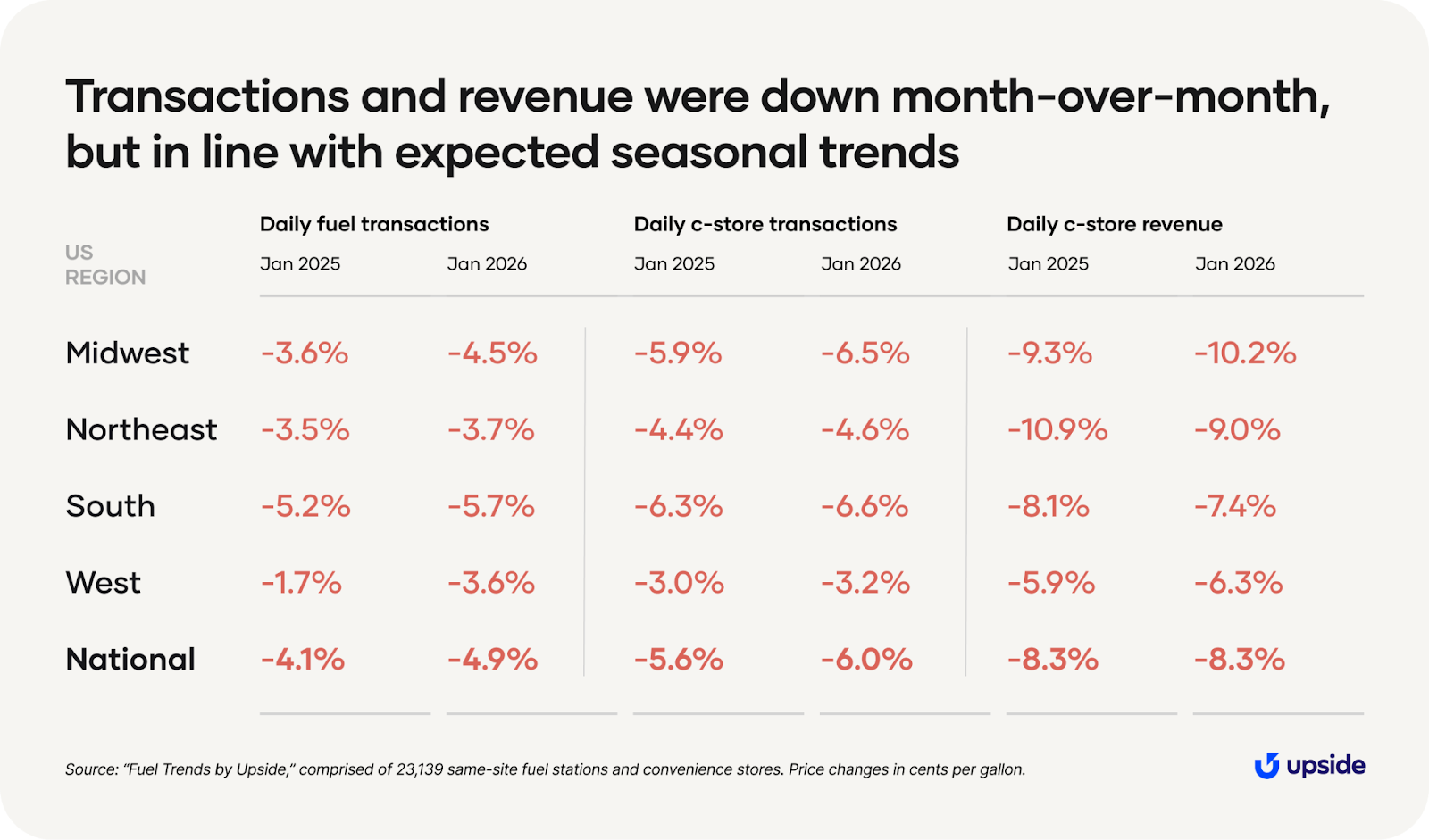

Nationally, fuel visits to the typical American station were down nearly 5%. C-store transactions, meanwhile, were down 6% and c-store revenue was down more than 8%. The fact that revenue declined more than transactions shows a pull-back in spending per visit.

Though it might feel like cause for concern, this is a predictable seasonal slowdown — and one we saw to roughly the same degree in 2025. As you can see below, the month-over-month decreases in January 2026 were remarkably similar to those a year prior. Changes in daily fuel transactions, daily c-store transactions, and daily c-store revenue per site were all within one percentage point nationally.

The wide-reaching impact of Winter Storm Fern

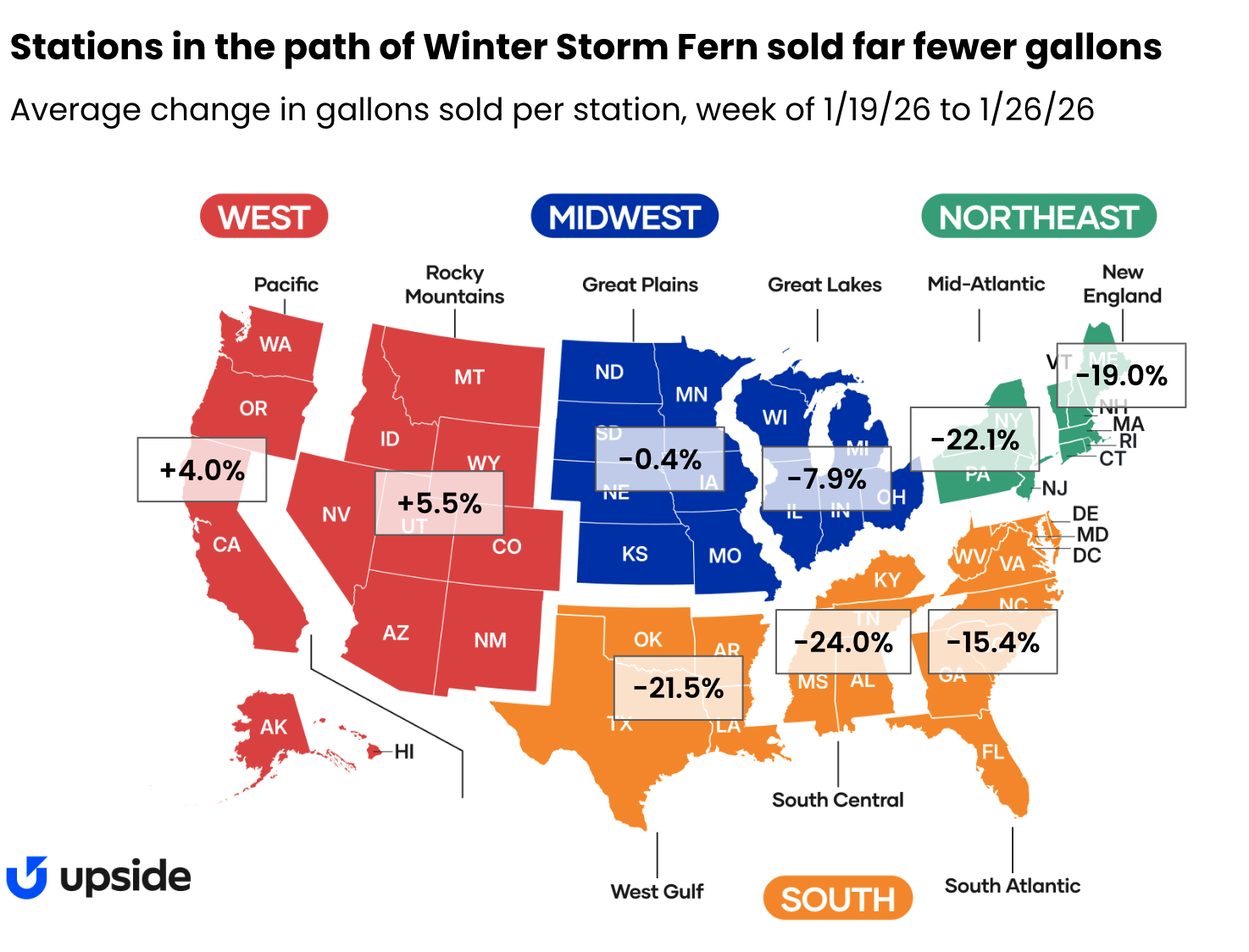

So, we’ve been talking about all these expected and typical seasonal trends. But for many Americans, January was by no means a typical month. Winter Storm Fern wreaked havoc across much of the country, ultimately affecting 230 million people with snow, ice, and exceptionally cold temperatures. In response, many drivers stayed off the road for multiple days.

The largest impact was in the band of states moving northeast from Texas to Maine. This disruption is shown clearly in the below map — note the double-digit declines in fuel demand in the South and Northeast.

So if this exceptional event occurred in January, how is it that the month overall was so similar to the year prior?

There are two reasons. First, Winter Storm Fern was a short-term event that did not disrupt the entire month. Second, January 2025 also experienced a cold snap, as we wrote about at the time.

Predictions and considerations

More visits, but tighter margins

In February, we should see improvement in fuel and c-store demand — both because of seasonal expectations and also continued recovery from Winter Storm Fern.

That will be welcome news to fuel retailers. What might not be as welcome, though, is the fact that oil prices continue to rise amid geopolitical tension. We expect rack prices to increase in February, leading to both higher sign prices and lower margins per gallon.

Potential tailwinds:

- Slowly but surely, the weather will begin to thaw across the U.S. in February. Warmer weather means more drivers on the roads, which means higher demand at gas stations and c-stores.

Potential headwinds:

- The U.S. labor market is cooling, with layoffs at their highest level to start a year since 2009.

- Peace talks between Ukraine and Russia appear to have stalled. Coupled with increasing instability in Iran, there are a lot of question marks in the global fuel supply. The uncertainty could lead to rack price increases.

- Although American military action in Venezuela may increase supply in the long run, the short-term impact is more likely to be supply disruption and market volatility.

Subscribe for monthly trend updates

Check out our insights hub with all our fuel and convenience monthly updates, or fill out the form below to subscribe to monthly fuel and c-store insights.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.