What we cover

Macroeconomic pressures are shifting consumer purchasing habits — and at May’s GroceryTech conference in Charlotte, industry leaders gathered to address how to keep winning trips from their shoppers.

Along with Ryan Draude of Giant Food, Upside’s Lindsey Kemmerich participated in a panel session titled "The income divide: Why grocery spend is diverging." The panel, hosted by Progressive Grocer’s Emily Crowe, focused on how to build meaningful loyalty across an increasingly fragmented shopper base.

The reality of the income divide

While high-level economic indicators suggest that aggregate consumer spending remains stable, underlying data reveals a significant divergence in shopper behavior.

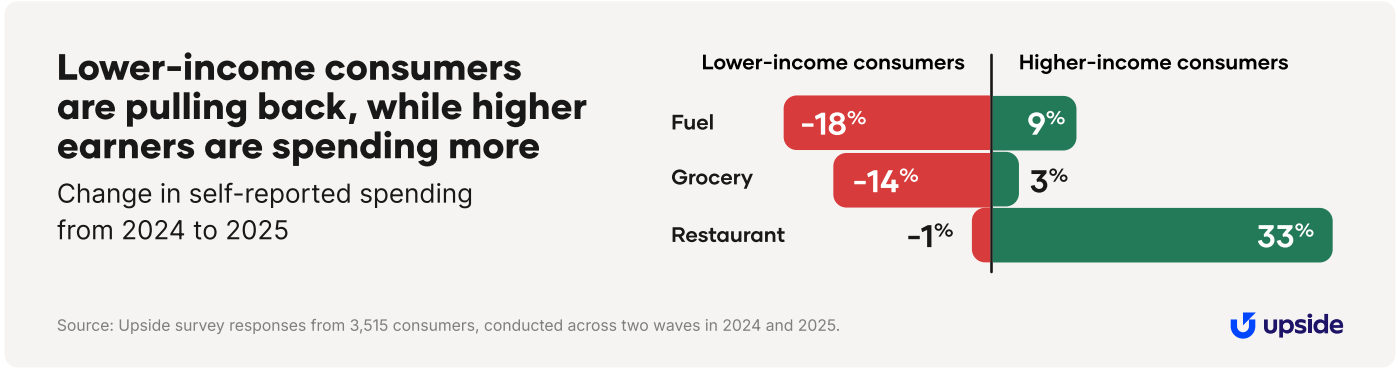

Findings from Upside's recent report, The Income Divide, demonstrate that consumer trends are splitting along the $75,000 annual household income line. Higher-income households report greater economic optimism and have increased their year-over-year spending across retail categories, including grocery, fuel, and restaurants. Conversely, lower-income households face severe economic strain and are pulling back significantly on non-discretionary purchases.

These divergences in shopping behavior are due in large part to diverging views about the economy. According to the report, 46 percent of higher-income shoppers view the economy as better than a year ago; on the other side of the line, 58 percent of lower-income shoppers feel the economy has worsened.

For Draude, a big concern is the danger of lower-income consumers shifting trips to other retailers and losing those consumers entirely.

“Once you lose them, all of you know how difficult it is to win them back,” he said at the event.

This spending gap is driven by long-term inflationary pressures. Since 2020, overall prices have increased by 26 percent, while grocery costs have surged by 30 percent. Simultaneously, higher earners have benefited from rising wages and rapid asset appreciation in real estate and financial markets, widening the financial gap between these two groups.

Redefining value for different audiences

The panel emphasized that value-seeking behavior isn’t unique to the lower-income segment, however. All consumers are seeking value right now, but they think about the search for value a bit differently.

“We see value-seeking behavior a lot even among higher earners,” Kemmerich said. “For some people, that might be a surprise. But at the end of the day, even if you can buy every single item at a premium, you might not do that. You're asking, ‘Is this item worth it? Do I want to spend money on that?’”

Higher earners prioritize convenience and product availability, focusing heavily on whether specific items are in stock. For this group, value is about experience optimization, and their primary question is whether a purchase is worth the cost. Interestingly, wealthier consumers are also highly likely to join loyalty programs to maximize their returns on selected purchases.

For lower-income shoppers, low prices are the primary consideration. This cohort relies heavily on discounts, coupons, and promotions to make ends meet, continually evaluating purchases based on immediate affordability.

Kemmerich noted that treating these groups identically creates significant margin risk. Retailers face the danger of over-discounting to higher-income shoppers who would buy items anyway, or under-selling lower-income consumers and causing them to skip shopping trips entirely.

Strategic responses: Winning the next trip

Customer relationships are highly fragile in the current environment. Approximately 90 percent of grocery shoppers are uncommitted, regularly split-shopping across multiple store banners to find the best deals. Because digital convenience makes it easy for consumers to cross-shop, grocery retailers must shift their perspective from winning permanent customer loyalty to winning the very next trip.

Draude shared how Giant Food navigates these shifting dynamics by leveraging personalization and maximizing the relevance of their loyalty initiatives. Traditional distinctions between price and quality are blurring, requiring grocers to offer flexible incentives.

Rather than relying on rigid, mass-market promotions that miss everyone, modern loyalty models must deliver tailored offers that match individual household needs. Personalized promotions solve this complexity at scale, ensuring that lower earners receive the value they need while higher earners remain engaged through experience and convenience.

Failing to adapt to this bifurcated market carries a steep operational cost. Grocers must move toward customer-centric models to capture incremental visits. With precise personalization, retailers can successfully bridge the income divide, earning one additional trip per month and driving sustainable revenue growth.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.