What we cover

Economic narratives — the stories we tell about where the economy is headed — carry enormous weight. They shape investment decisions, consumer behavior, and business strategy. But narratives that aren’t grounded in data can be misleading.

The question worth asking right now is: which narratives are meeting economic reality, and which ones aren't?

I’ve had the privilege of sharing my answer to that question with NACS on two different platforms recently: first on stage at NACS State of the Industry Summit, and then on its Convenience Matters podcast.

Read on for my thoughts about the current economic environment — how we got here and where things might move in the future.

Storytelling: The unexpected influence on the economy

There are fundamental indicators and key statistics that tell us about how the economy is performing. You’re likely familiar with many of them — like GDP, the inflation rate, and unemployment rate, to name a few. These objective statistics help guide the decisions of business leaders, policymakers, and investors all over the world.

But humans are emotional creatures, and our world is anything but objective. Most people might not think of economics that way, but remember that it’s a social science. In all areas of life, people are moved by compelling stories, and economics is no exception to that rule.

In real life, those fundamental indicators and those compelling narratives combine to shape our perception of the economy. That statement is especially relevant in our current economic environment.

The U.S. economy is currently supported by three pillars: the labor market, artificial intelligence, and consumer spending. Two pillars, the labor market and consumer spending, were doing most of the work a year ago. AI is newer — and harder to predict. Here's what convenience retailers should know about all three.

The labor market is healthy, but uneven

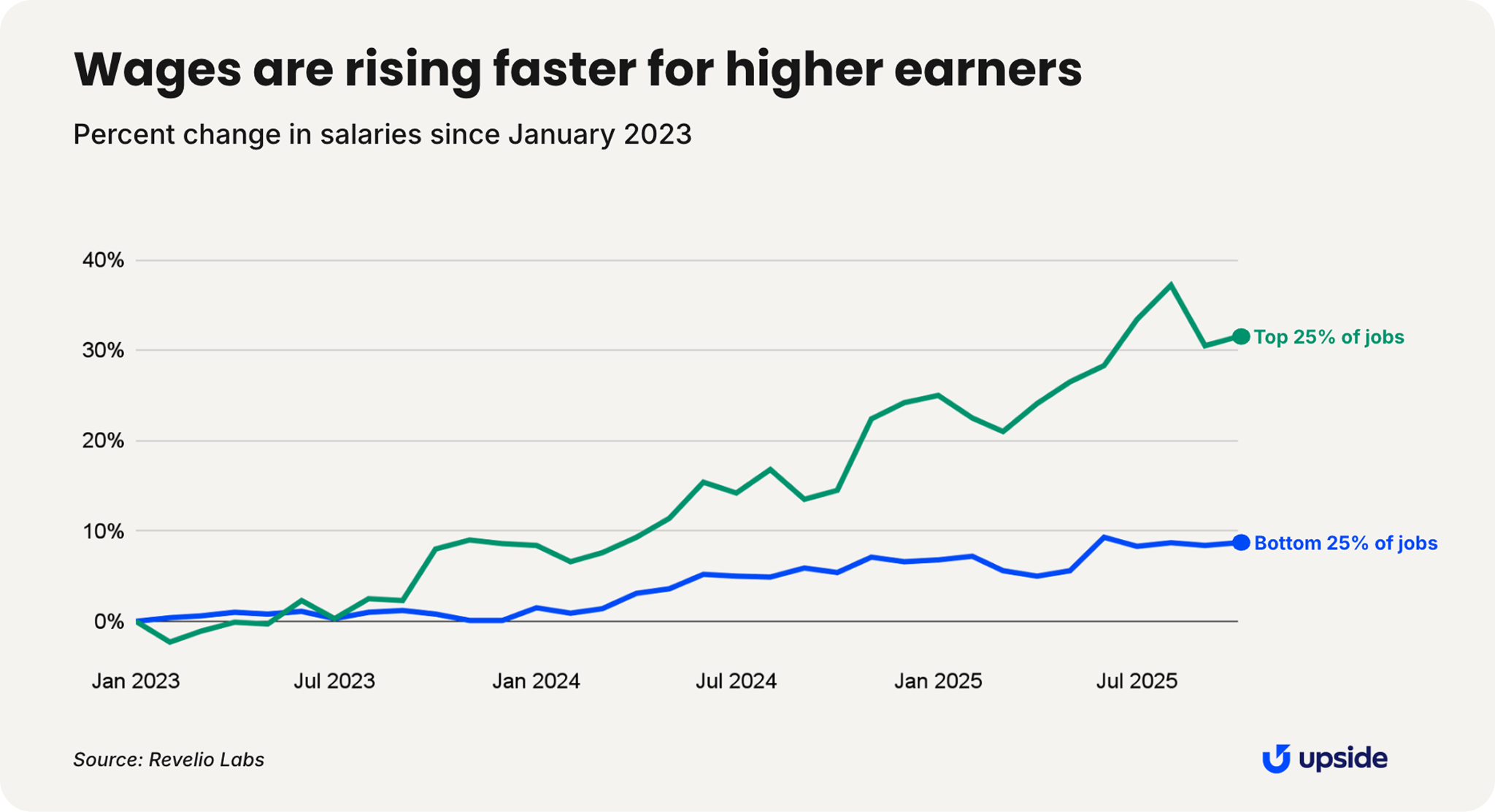

First, the good news: Inflation-adjusted income has grown by up to 2% for the median worker over the past two years.

However, that growth is disproportionately concentrated among high earners. Lower-income workers are seeing slower wage gains while absorbing more of the impact of inflation, a pattern that economists call the K-shaped economy, and one that shows up repeatedly in the data right now.

The job market itself has effectively frozen. Companies aren't laying off workers, but they're not hiring, either. This "low-hire, low-fire" environment constrains growth, since economic expansion typically depends on rising employment. While it is possible to grow without increasing headcount, it's harder to do so.

AI is driving narratives, not results — for now

Here is where stories have really come into play as of late. AI investment has surged since 2023, delivering tremendous growth to the stock market.

Prior to that surge, growth in the stock market and growth in the labor market moved in lock-step. But since, they’ve de-coupled — that investment is flowing into companies and data centers, but not into hiring. This dynamic benefits asset holders more than workers, deepening the K-shape further.

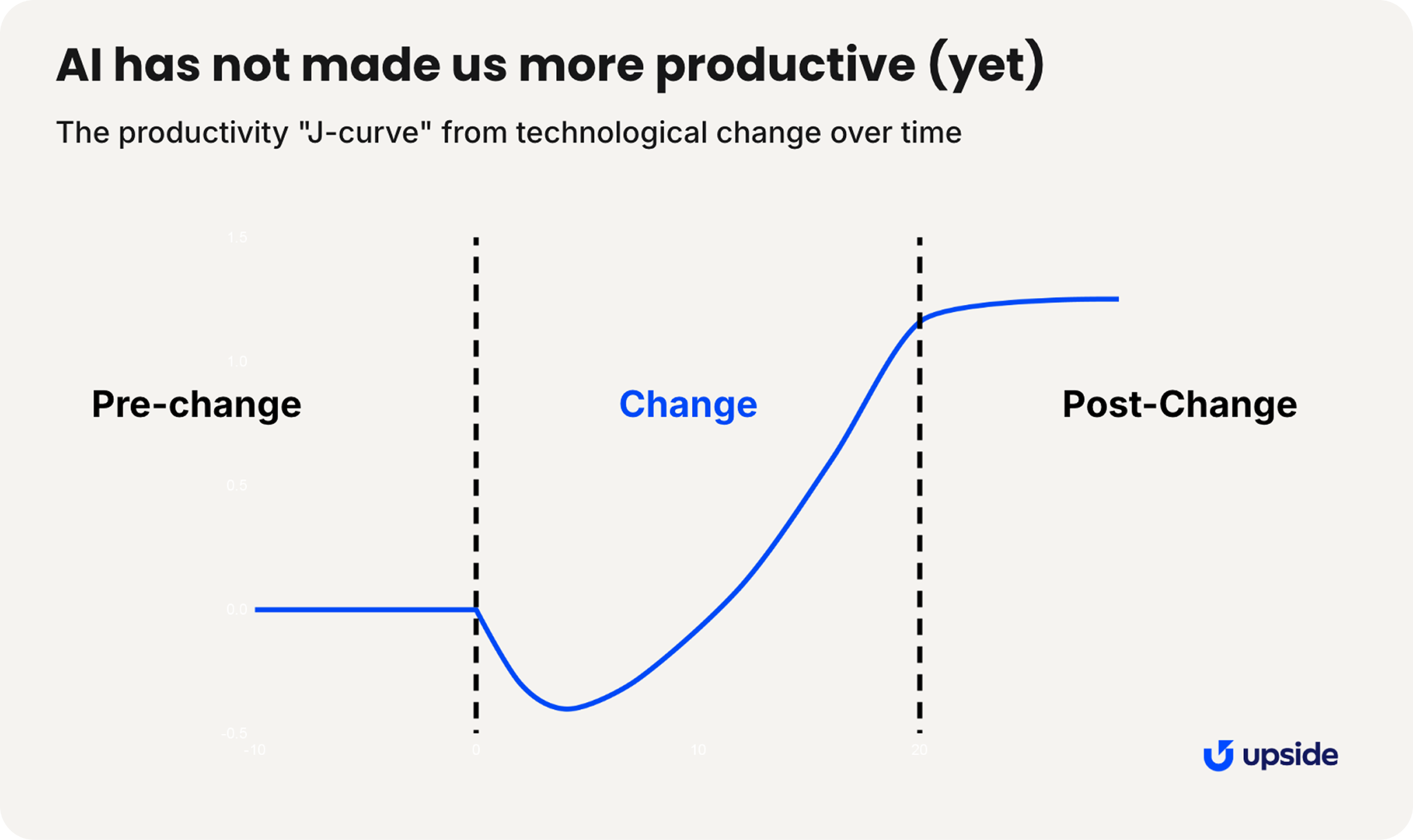

At the aggregate level, AI hasn't meaningfully moved productivity numbers yet. This result follows what’s known as the “productivity J-curve.” New technologies often cause a temporary dip in productivity as organizations invest in learning, infrastructure, and implementation before the payoff comes. That's where most companies are right now — still figuring it out, still in the change period.

The bigger question is when the AI economic narrative will meet economic reality. Right now, the promise of AI is real, but the timeline is still unclear.

Tariffs are compressing margins, and consumers feel it

Any discussion of the third pillar, consumer spending, has to include policy. Policy shapes what consumers can and can't afford to do. And in this administration, tariffs are the policy directly impacting consumer spending.

The current effective tariff rate of 10.5% has raised consumer prices by an estimated 0.6%. This increase translates to roughly $850 per household per year in lost purchasing power. That may sound modest, but measured against a typical retailer's net profit margin, it becomes more dramatic quickly.

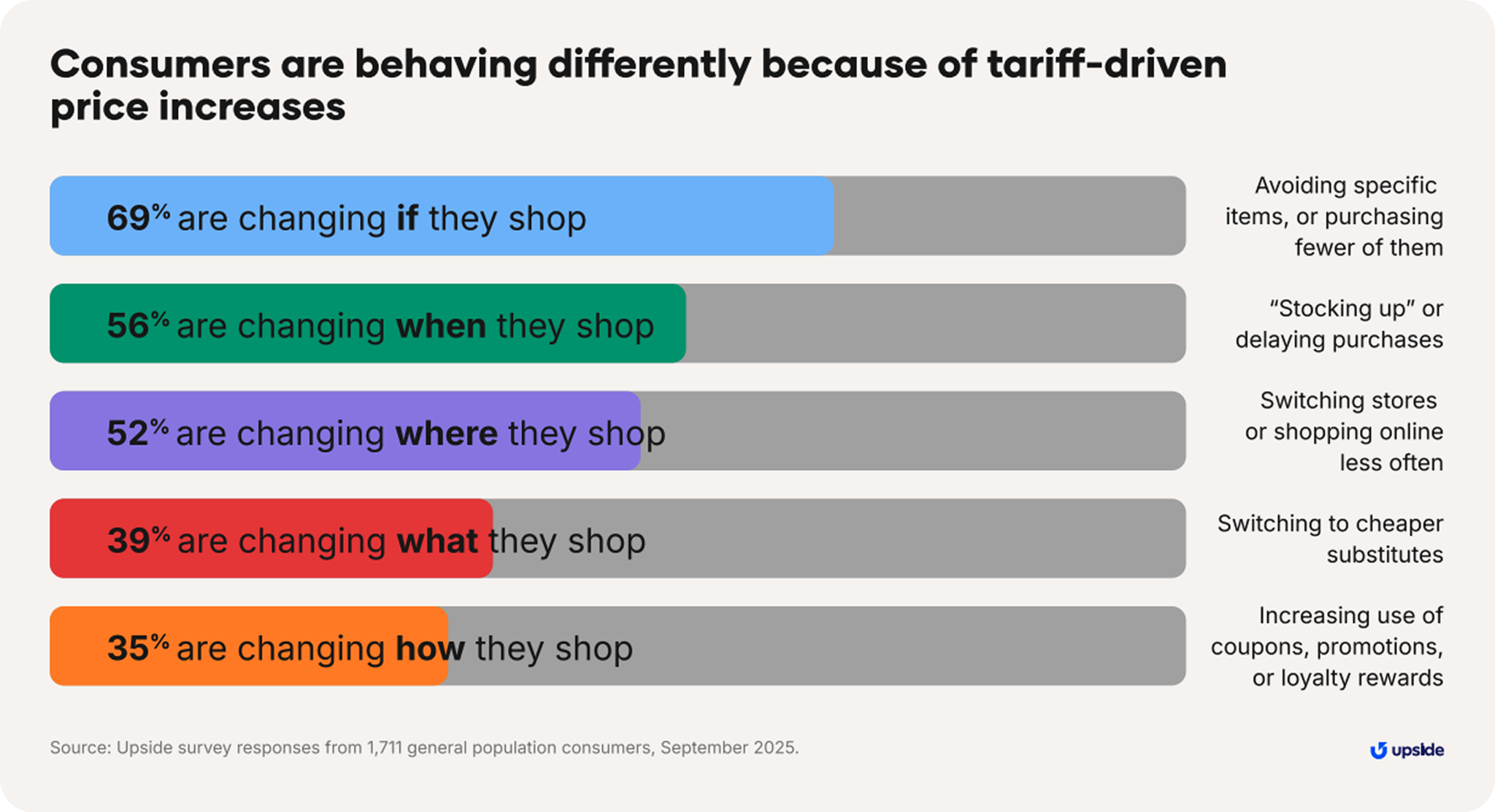

Consumers are aware of the loss, too. In a survey conducted through Upside, 79% said they've already changed their shopping behavior in response to tariffs. That's a higher number than expected. Add to that an inflation rate that has now sat above the Federal Reserve's 2% target for five years, and consumer sentiment that just hit a 50-year low, according to University of Michigan data.

Historically, retailers have absorbed 80 to 90% of tariff costs through compressed margins. Early data from the current round of tariffs suggests a similar pattern. But, with gasoline above $4 a gallon, consumer sentiment and shopping behavior are likely to worsen before they improve.

What this means for fuel and convenience retailers

Every administration faces a trilemma. It can realistically pursue two out of three goals — economic growth, low inflation, or a specific trade or fiscal policy — but not all three at once. Tariffs are the clearest current example of that trade-off in action. Prioritizing tariffs pulls against both economic growth and low inflation, and it's retailers who typically feel it first. For fuel and convenience operators, that means the policy environment itself is a margin headwind.

Upside transaction data bears this out. Convenience store revenue grew 0.6% year over year — but food inflation rose 2.5% over the same period. Grocery stores and restaurants show the same pattern: nominal revenue up, but well below their respective inflation benchmarks. Most of that revenue growth is price-driven, not demand-driven.

It shows up in retailer sentiment, too. In a survey of fuel and convenience operators, cost management has replaced labor as the top concern heading into 2025. The top three challenges cited in Q1 were inflation, tariff-related costs, and supply chain disruptions. Where operators a year ago were focused on finding and keeping workers, today they're focused on protecting margins.

When we dig into consumer spending a little more, the K-shape appears again. Lower-income consumers report cutting back across fuel, convenience, grocery, and restaurant spending. Higher-income consumers report increasing spending across all of those same categories. Overall spending looks fine in aggregate — but it isn't evenly distributed, and that distinction matters for how retailers think about their customer base.

The future outlook

The probability of a recession in the next 12 months is elevated — somewhere around 40% by my prediction, compared to a historical baseline of 10% to 15%. Slowing consumer spending, an uncertain AI trajectory, and an energy-cost headwind justify caution.

Fuel and convenience retailers are optimistic. In our recent survey, 80% of fuel and convenience retailers said they expect their business to grow in the next six months. It’s of industry optimism that the data, on balance, still supports.

The overall economy is being propped up by three columns. Two of those columns, the labor market and consumer spending, are still supporting economic growth. But there are some cracks showing, and they’re cracks worth monitoring.

Want to hear more? Check out my recent podcast appearance on Convenience Matters, presented by NACS.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.