What we cover

What a month.

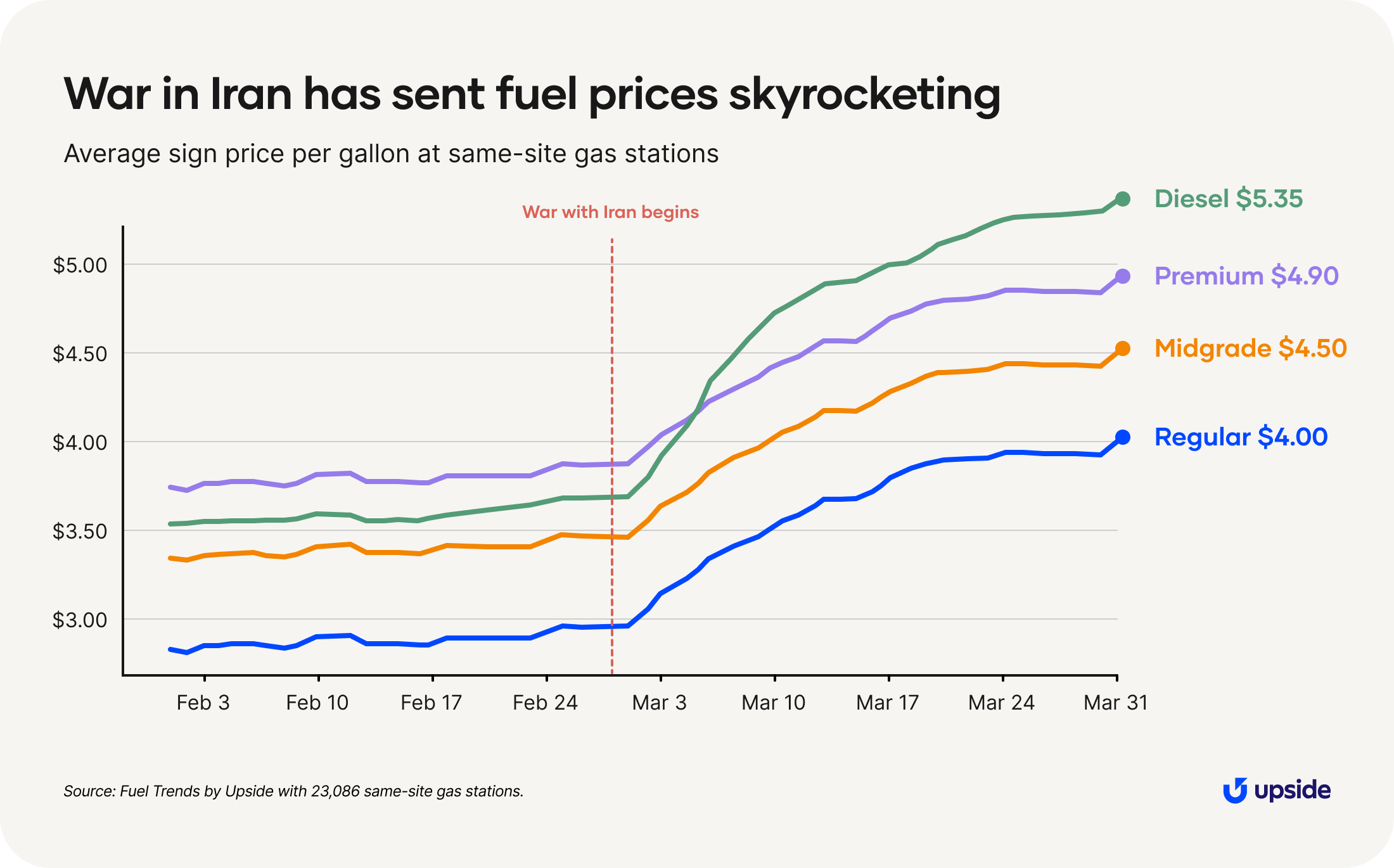

You know the story well by now, but we’ll record it here for posterity. On the final day of February, the United States attacked Iran, and in response, Iran effectively closed the Strait of Hormuz, a critical oil and gas chokepoint. With roughly 20% of the world’s fuel supply stuck in the Persian Gulf, prices for oil (and thus, gasoline and diesel) have ballooned in just a few weeks. At time of publishing, regular gas prices are comfortably above $4 per gallon.

The effects of the war and the Strait closure are wide-ranging, and we’ll cover all of them here in addition to our usual month-over-month tracking.

As usual, we’ll start by comparing March to February. Though in this particular case, we’re basically talking about two different worlds.

Last month’s data

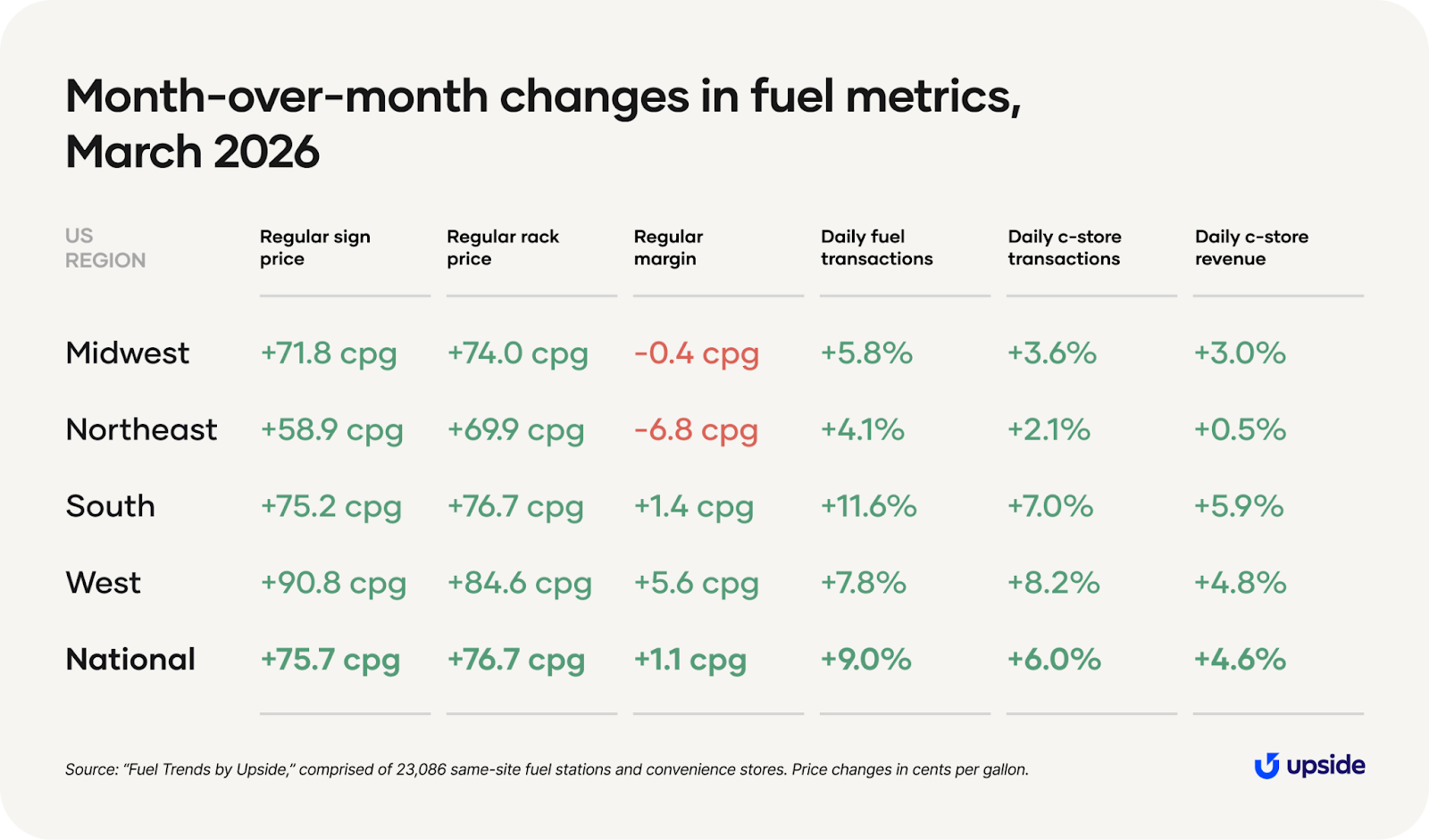

Prices skyrocket — and transactions rise, too

The effective blockade at the Strait of Hormuz began on the final day of February, and it persisted through the entire month of March. That drove up oil prices — and with them, gas prices. You can see those impacts above.

From the end of February to the end of March, West Texas Intermediate oil futures increased from about $67 per barrel to $103, according to the Energy Information Administration. That’s a 54% increase in just a month.

The resulting gas price changes were just as stark. The average American rack price was up by 77 cents per gallon from February to March. And while sign price changes usually lag behind their rack price counterparts, fuel retailers had little choice but to lift sign prices rapidly to cover their significantly increased costs. Sign prices were up by about the same amount in March — 76 cents per gallon.

Taken together, margins across America held steady month-over-month. That’s important, because some drivers inaccurately accuse fuel retailers of price-gouging during high-price times like these.

A few regions experienced trends that differed from the national average. The Northeast has the lowest increase in regular grade rack prices month-over-month, as well as the lowest increase in sign prices. That meant the typical Northeast station saw a 7-cent drop in margin. It’s unclear why; however, we anticipate Northeastern stations will see larger jumps in sign price than its neighbors in the near future.

Additionally, the West saw the highest increases in both rack price and sign price, leading to a modest 6-cent increase in margin. The rise in prices is likely due to parts of Southern California being the first area to switch over to summer-blend gasoline. The margin, however, is likely just a correction to the roughly-equivalent drop we reported last month.

When combined, the two regional trends seem to cancel each other out at the national level.

Now, with prices so high, you might expect that transactions would drop, because fewer people would want to pay for expensive gas. But the opposite occurred — fuel transactions were up 9% in March, a considerable gain. Why?

The impression that people would change their behavior because of high gas prices is right. But rather than buying less gas, consumers try to reduce the sting of huge totals at the pump by making smaller transactions more frequently.

Our data shows this is exactly what happened in March.

What kind of impact is this behavior change having on station volume? Though people are buying fewer gallons per trip, our data shows volume is not down. Yes, behavior is changing, but demand is relatively inelastic in the short term. People still have to commute to work and take their kids to school. Plus, seasonal factors play a role; the roads get busier as the weather gets warmer.

Though as you can see below, volume is not increasing by nearly as much as transactions are.

Meanwhile, just as fuel transactions increased, so did c-store transactions. Inside the store, visits were up to the tune of 6.0% nationally. Once again, we can point to similar seasonal trends with higher demand amid spring weather.

But demand isn’t up across the board. Customers are indeed cutting back, and they’re doing so in an area that’s particularly painful for retailers.

“Octane’s razor” — demand for higher grades falls

As we’ve covered, fuel prices have increased to dramatic levels over the past few weeks. Each grade — regular, midgrade, premium, and diesel — is up by more than a dollar per gallon from early February levels.

Diesel experienced the greatest jump in price, and it has actually overtaken premium as the most expensive grade at this time. Diesel buyers usually don’t have a choice but to use diesel, however, so we haven’t seen much impact on diesel demand this month.

We can’t say the same for midgrade and premium fuel. As these gas grades became more expensive, consumers started trading down, swapping out those more expensive options for regular gas. Today, we see that premium and midgrade sales are dramatically down since the start of the war, while regular sales are rising.

Consumers get used to the price they generally pay at the tank. If it usually costs, say, $50 to fill up, tacking on an extra $20 can be a shock to their system.

And their change in behavior is also a shock to retailers’ operations. Since these elevated fuel grades are usually more profitable for retailers, it’s a meaningful change. Earlier we covered how regular margins are essentially unchanged in March. And though they’re still generally healthy, losing higher-margin premium gallons is a trend worth watching in the coming months.

Predictions and considerations

All eyes on the Strait

Forgive us for stating the obvious, but the only thing worth mentioning here is the Strait of Hormuz.

Re-opening the Strait would be the single-largest tailwind for the fuel industry, while remaining closed would be its biggest headwind. Shortly before publication, the United States and Iran publicly agreed to a two-week ceasefire. The market responded in kind, with the price of oil plunging on the news.

We’re far from the finish line; trust between the nations is low, so this ceasefire is fragile and could fall apart at any point. Further, the U.S. and Iran have made contradictory statements about the re-opening of the Strait of Hormuz. The White House expects a full and immediate re-opening of the Strait, while Iran wants to charge each vessel a fee for passing through.

The crisis is not over, but hopefully we are on a path toward deescalation and stability.

Potential (other) tailwinds:

1. Continued warming weather will provide further boosts to demand for both gas and c-store purchases.

2. Early in April, OPEC announced its members will increase production in May by 206,000 barrels per day. What remains to be seen, however, is whether the oil can actually reach the market. Many OPEC members are located on the Persian Gulf and require passage through the Strait.

3. Several countries will continue releasing oil from their strategic petroleum reserves, including the United States.

Potential (other) headwinds:

1. In addition to price increases driven by the supply shock, seasonal factors are also driving prices up. That’s due to the impending switch-over to more expensive summer-blend fuel.

Want a closer look at the data?

Our team is closely following the war in Iran and its impact on global oil markets. For regular updates and video explainers, visit our Strait of Hormuz Impact Hub.

Check out our insights hub with all our fuel and convenience monthly updates, plus special industry reports.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.