Card issuers boost engagement and spend with Upside

More value with no added complexity

Credit and debit card issuers — FinTech platforms and traditional banking institutions alike — already invest heavily in cardholder rewards to engage their users and build long-lasting customer loyalty. But as competition for daily spend intensifies, even the strongest programs are looking for new ways to drive deeper engagement, especially in essential, high-frequency categories like food or fuel.

This creates an opportunity for card issuers: to deliver more value where it matters most — everyday purchases — without adding operational lift. To achieve it, many top platforms turn to Upside.

Personalized promotions, seamlessly integrated

Upside enables card issuers to embed always-on, personalized cash-back offers directly into their cardholder experiences. There’s no need to build a rewards program from scratch — Upside has already done the work.

Our platform powers the highest-value offers in everyday categories like fuel, grocery, and dining by ensuring each promotion drives incremental profit for retailers. This means partners can:

- Deliver more value to cardholders through relevant, seamless rewards

- Influence real–time spend at the moment of purchase

- Reinforce top-of-wallet positioning without added complexity

- Access actionable insights into program performance

And the benefits for consumers are clear, too. Upside helps shoppers earn 3x more cash back on everyday purchases compared to competitors — giving them more reason to reach for your card first. But what actually happens when issuers partner with Upside to offer more rewards to their users? The proof is in the numbers.

To answer the question above, we studied 45,000 cardholders from two issuer partners — one gig economy payment app (debit card), and one top mobile banking app (debit and credit). We analyzed the behavior of these cardholders at a national fuel retailer before and after they started using Upside.

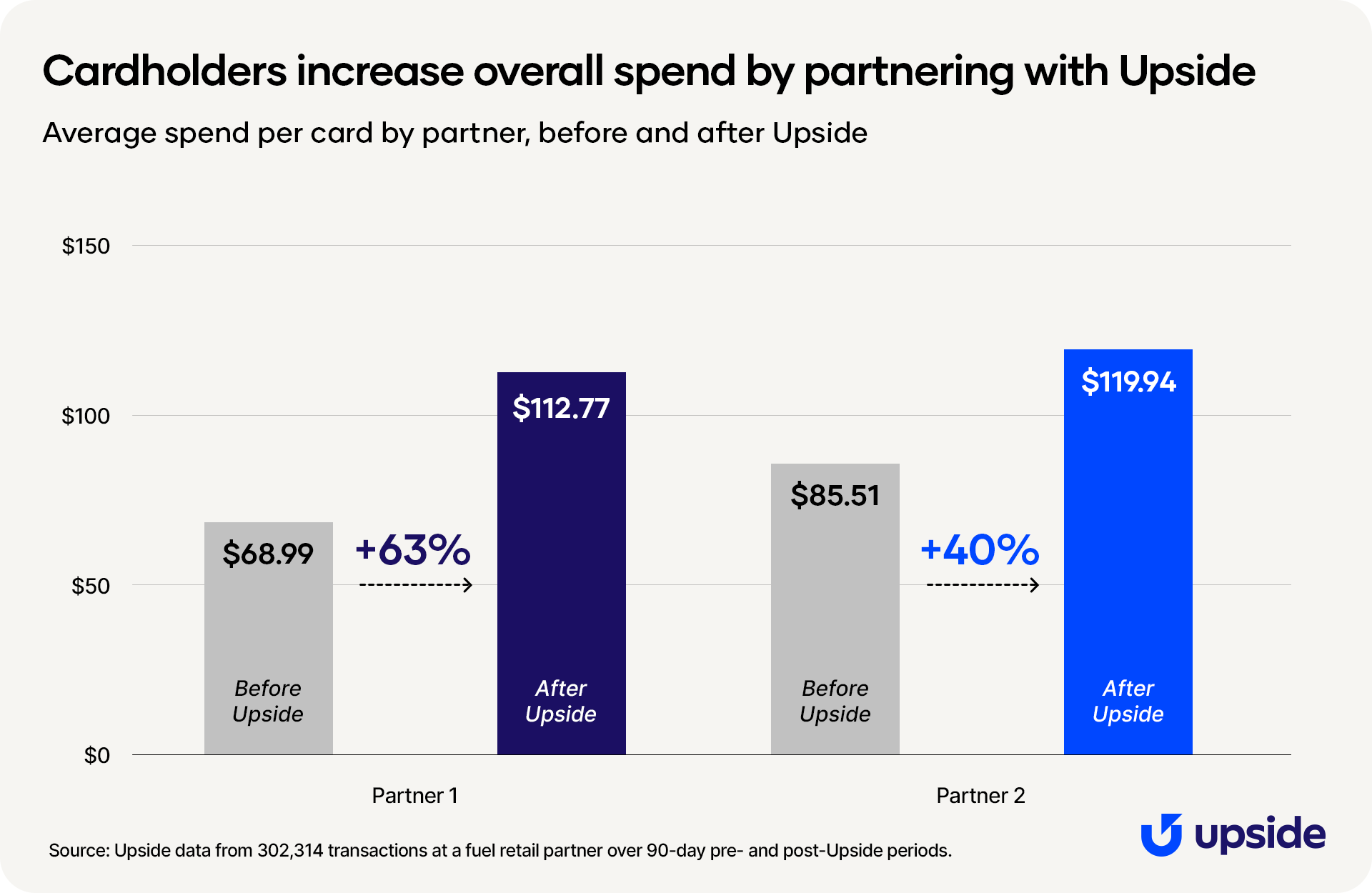

Double-digit growth in cardholder spend

When these providers integrated Upside’s personalized promotions into their digital experiences, cardholders responded immediately.

First, customers started visiting this fuel retailer more often. After introducing Upside offers, one partner saw a 26% increase in transaction frequency, while the other saw a 54% increase — clear evidence of stronger engagement.

And not only were cardholders visiting this fuel retailer more often, but they were spending more when they did. Each partner saw an increase in average transaction size when its cardholders visited the fuel retailer.

But ultimately, issuers are looking to increase spend — ensuring that their customers reach for their cards in their wallets first, winning as many dollars as they can. By increasing both transaction frequency and transaction size, average spend per card naturally increased, as well.

Why it matters

Most consumers decide which card to use based on the rewards they’ll receive from a given transaction. By embedding Upside’s offers, issuers can give their cardholders a reason to put their brand first at checkout.

Partnering with Upside drives more transactions, stronger retention, and deeper long-term engagement, all while delivering sustainable, measurable ROI.

Make your card the go-to for everyday spend.

Learn more at upside.com/partnerships or reach out to partnerships@upside.com.

.jpg)