What we cover

The retail marketplace is consolidating, with massive players like Walmart and Amazon gobbling up market share from mid-size retailers. Consider that in Q2 2023, Walmart was responsible for almost 36% of total online grocery sales in the U.S., a increase of five percentage points year-over-year.

As a result, mid-size retailers have had to get creative in their hunt for customer transactions. Some retailers answer the call by strengthening their commitment to their loyalty programs, expecting repeat, loyal shopping to boost transaction frequency and basket size.

Is loyalty a solution to help mid-sized retailers keep (or grow) their market share?

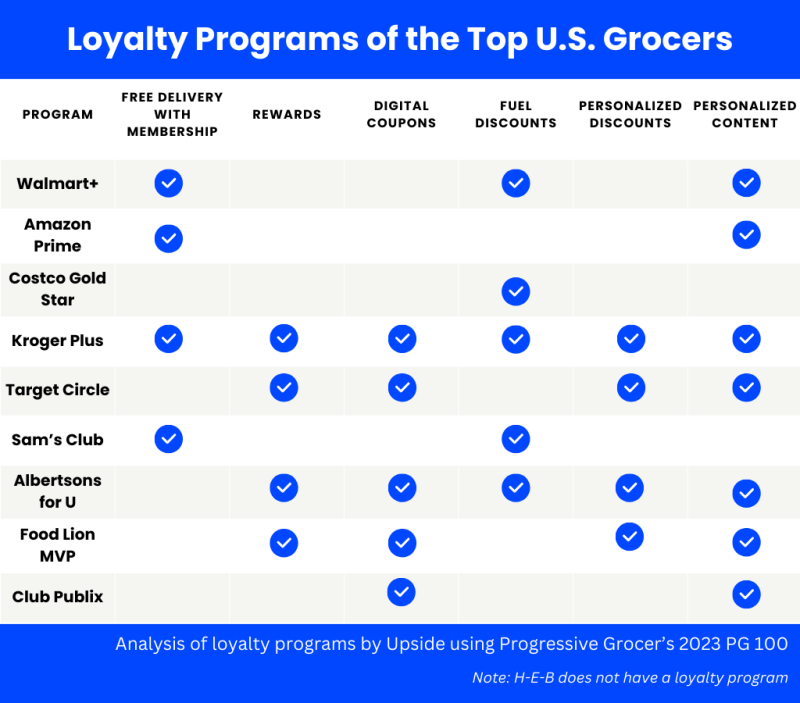

We reviewed the loyalty programs from the "Big Five" grocery retailers in the U.S. (Walmart, Amazon, Costco, Kroger, and Target), along with four others we consider “best-in-class,” to see if successful loyalty programs drive more market share.

What are grocery loyalty programs and why do they matter?

Grocery store rewards program are a key strategy for retailers to encourage repeat visits and increase customer lifetime value. These programs typically offer points, discounts, and personalized offers in exchange for customer data and shopping frequency, delivered through mobile apps, digital cards, and integration with your existing point-of-sale systems.

Most grocery store rewards programs include digital loyalty cards and mobile apps, points-based reward systems for future discounts, exclusive member pricing on select products, and partner rewards that extend value beyond grocery purchases.

However, despite your investment in program features and benefits, loyalty programs have some gaps when it comes to impacting customer behavior and business outcomes.

While loyalty programs remain necessary to meet customer expectations, and do provide value in customer retention, their impact on driving new growth may not be as significant as retailers expect. The question isn't whether grocery store rewards programs matter — it's understanding their role within a broader customer acquisition strategy that can deliver the competitive advantage retailers need against consolidating market leaders.

The problem: Loyalty membership doesn’t equate to loyal behavior.

Many retailers have dedicated extensive resources to differentiate their loyalty programs and provide the best experience for their customers. These programs are often highly sophisticated, and many of them have driven real value — encouraging repeat business, providing grocers with valuable customer insights, and creating new opportunities for customer engagement.

But loyalty programs have become table stakes to the modern shopper — things that they’ve come to expect from their preferred brands.

Data shows that today’s average shopper has 18 loyalty programs on their mobile device; two to three of those are for grocery brands alone. Related data from FMI shows that the average grocery shopper frequents five different banner stores, notably more than the number of loyalty programs they belong to on average.

So if these loyalty programs aren’t defining their shopping routines, what is? In a recent Upside survey, grocery customers said that a store's distance away from them is 3.2 times as important as whether that store has a loyalty program.

The result: Grocery loyalty programs have mixed financial benefits.

For the top 10 grocery retailers in the U.S. — those with the most resources and influence to drive customer loyalty — there is no clear connection between the loyalty programming they use in-market and fiscal growth.

Our research shows minimal revenue increases over time for grocers with loyalty programs, paid or free. While the research did find a positive correlation between app downloads and revenue, it’s not enough to imply causation.

Even more surprising, those retailers with a paid membership program experienced slower growth in the past year relative to those with a free loyalty program.

To be clear, these loyalty programs are necessary. As noted above, customers expect them as part of their shopping experience. While these programs may safeguard market share, they are doing little to expand it.

The problem: Loyalty programs are all fairly similar.

Today’s loyalty programs offer fairly similar benefits to members, no matter which retailer you consider. Need proof? Try searching online for the “best loyalty programs.” You’ll surface a handful of “top-10” lists, but the publications lack any real consensus. Each list mentions different stores with similar perks.

This phenomenon held up in Upside’s research on the top retailers and their loyalty programs, as well. As you can see, there’s a practically interchangeable list of features, without industry standards or proven effectiveness from one program to another.

The result: Loyalty is becoming an arms race.

In the sea of nearly identical programs, grocers are racing to keep up by adding perks such as free delivery or bigger buy-one-get-one savings. The nature of an arm race is that entities are all fighting for the same thing — in this case, a finite number of customers — but individually spending more money than what they will be able to recoup.

These additional program “perks” often end up costing retailers much more than traditional points-based loyalty programs do. These offers overshadow any return on investment that loyalty programs might provide, with retailers essentially overinvesting in a portion of their customer base.

One way for retailers to cover the cost of these added perks is by charging customers additional fees or subscriptions—and bigger corporations have an advantage here. Market leaders like Walmart, Amazon, and Costco have a de-facto lock on fee-based loyalty (think Amazon Prime). And since their participating shoppers are unlikely to invest in other programs that require membership fees, these conglomerates have a stronger grip on customer spending.

Loyalty programs can be upgraded and augmented internally as much as a retailer can afford. But by their nature, these programs often cannibalize expected sales and do not provide a positive return on investment.

The verdict: Retailers need a loyalty boost.

Let’s return to our original question: Is loyalty programming the solution to help mid-sized retailers keep (or grow) their market share?

In short, it’s not likely.

Retailers must ask themselves two pivotal questions when contemplating loyalty as a strategy for expanding their market share:

- “Will adding more perks to my loyalty program differentiate my business for customers who are part of multiple loyalty programs already?”

- “If I invest more in my loyalty program, will I eventually receive a clear and measurable return on that investment?”

If the answer to either of these questions leans toward "no," then channeling more resources into existing loyalty programs is a risky way to protect against the encroachment of emerging rivals.

Loyalty programs are valuable tools for targeting existing customers and those for whom your locations are conveniently situated. But reflecting on the data presented, loyalty programs alone don't provide the guaranteed path to success for mid-sized retailers trying to compete with Walmart-sized retailers for market share.

To compete effectively against Amazon and Walmart, retailers must think, "loyalty and..." In other words, they need both loyalty and other strategies that expand their brand’s reach, and include consumer behavior. Digital marketplaces with dynamic and personalized incentives for each customer are an example of that.

Retailers have the opportunity to win more wallet share by tapping into ready-made customer networks of hungry shoppers deciding where to buy. There are a number of marketplaces with massive built-in user bases, acquired and retained through their own advertising and marketing spending so our retailers don’t have to. These marketplaces introduce their user base to participating retailers, and incentivize them to choose participating retailers instead of their competitor.

In this increasingly consolidated market landscape, marketplaces are a good start in engaging the shoppers who don’t know those retailers today, and introducing them to everything that makes the retailers’ store worth visiting again… and again, and again.

Upside: The performance-based approach

The evidence is clear: your traditional grocery store rewards program alone isn't enough to drive sustainable growth. If you recognize this reality, you need complementary strategies that enhance your existing loyalty investments rather than replace them entirely.

This is where performance-based incentives become necessary for your business. Unlike traditional marketing approaches that charge you for impressions or clicks, performance-based solutions tie all compensation directly to measurable business outcomes — specifically, incremental transactions and profit that wouldn't have occurred otherwise.

Performance-based approaches offer you proven incremental impact through rigorous test-versus-control measurement methodology. You only pay for verified results, not marketing activity. These strategies enhance your loyalty program performance by driving new customers into your existing reward systems while providing competitive differentiation through personalized offers that don't affect your posted pricing.

Upside's marketplace model exemplifies this approach by connecting you with nearby consumers through personalized cash back offers. Upside is already a destination for consumers making everyday purchases like groceries or meals at restaurants. Rather than competing with your existing grocery store rewards program, Upside complements it — driving new customers who then become candidates for your loyalty program enrollment while increasing visit frequency and spend among your current members.

The results speak for themselves: participating grocery retailers see measurable increases in same-store sales without increasing operational costs. Most importantly, you only invest when you receive proven incremental profit, eliminating the risk that has traditionally accompanied customer acquisition efforts.

For mid-sized grocery retailers competing against market consolidation, this means expanding to include growth strategies that deliver accountable, measurable results.

Frequently asked questions

How often should I update my grocery store rewards program?

Grocery store rewards programs work best when updated strategically rather than constantly. Most retailers find success by monitoring key metrics like redemption rates and customer engagement, then making targeted improvements based on the data.

What's the typical cost of running my grocery store rewards program?

Program costs vary based on complexity and reward structure. The key question isn't your total cost but whether your program delivers measurable return on investment. Performance-based alternatives can eliminate your upfront risks by charging only for proven results.

How does my grocery store rewards program actually impact customer behavior?

While your grocery store rewards program meets customer expectations, driving exclusive loyalty to your store requires additional strategies. The average grocery shopper belongs to multiple loyalty programs while spreading purchases across different retailers monthly. This means your program membership doesn't necessarily translate to concentrated spending at your locations. You should recognize your loyalty program as an important foundation that works best when paired with customer acquisition strategies that drive incremental business to your stores.

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.