Tracking retail fuel trends: September 2025

The change in season brings two expected developments to gas stations: a downturn in demand and a cheaper blend of fuel.

Dr. Thomas Weinandy

Tracking retail fuel trends: September 2025

The change in season brings two expected developments to gas stations: a downturn in demand and a cheaper blend of fuel.

September marks the end of summer, which indicates that the busiest time of the year for fuel retailers has come and gone. Booming summer months help to create a cushion during slower winter months — but it’s not all bad news for fuel operators.

Midway through September, most American fuel retailers are allowed to make the seasonal switch to a cheaper blend of fuel, lowering sign prices and helping to soften the expected downturn in transactions. In this month’s Fuel Trends update, we’ll explain why this happens and take a closer look at the impact of that switchover.

Last month’s data

A drop in demand, softened by lower prices and better margins

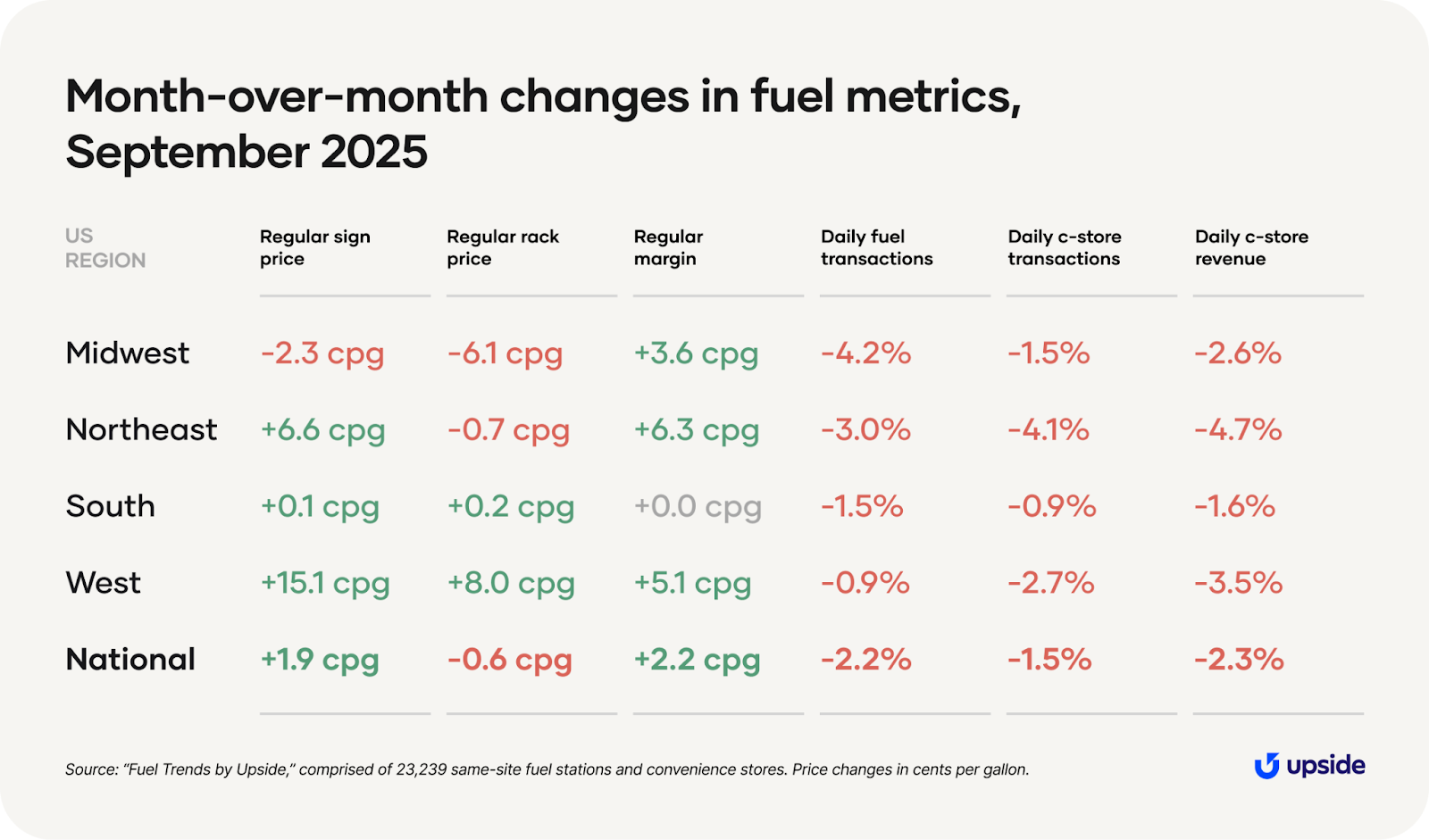

Relative to August, regular pump prices in September were 1.9 cents per gallon higher at the typical American station. It’s a modest increase that was driven by substantial gains in the West, where month-over-month prices increased by more than 15 cents per gallon.

We can pinpoint a few events as the causes — first, we saw higher-than-usual refinery maintenance in Southern California, which reduced supply and increased rack prices. A pipeline outage in the Pacific Northwest did the same, and retailers passed on those costs to consumers in the form of higher sign prices.

In the largest markets of the region, sign prices actually rose even more than the average:

- +15.2 cents per gallon in Seattle

- +17.9 cents per gallon in Portland

- +19.4 cents per gallon in Los Angeles

- +18.8 cents per gallon in San Diego

Despite the increase in sign prices, profit margins managed to tick up a slight amount nationally — 2.2 cents per gallon, on average.

Now, let’s turn to monthly demand. Although the price changes outside of the West Coast were small, demand dipped in all regions of the US as part of the expected seasonal declines. Nationally, fuel transactions were down by more than 2%, with steeper drops in the Midwest and Northeast. Meanwhile, convenience store transactions were down 1.5% nationwide, with the Northeast seeing the biggest month-over-month declines. C-store revenue dropped even more than transactions, declining 2.3% per store nationally.

Diving deep on the seasonal switchover

September is an important month for the fuel industry because most of the country switches over to the cheaper winter blend of gasoline after September 15th. We’ve mentioned this seasonal switchover in past recaps, but here, we’ll explain in further detail.

During the warmest months of the year, the Environmental Protection Agency requires that gas stations sell a more expensive blend of fuel. What’s different about it? Because the volatile organic compounds within gas can more easily evaporate in warmer weather, so the summer blend requires more complex (and expensive) refining.

The level of concern is lower in the colder winter months, so most of the country switches over to their winter-blend fuel after September 15th. (It then stays in circulation until the end of May.)

However, some hotter regions of the country use summer blend gasoline for longer. For example, Phoenix, Northern California, and parts of Eastern Texas use the summer blend through the end of September; Southern California uses it through the end of October.

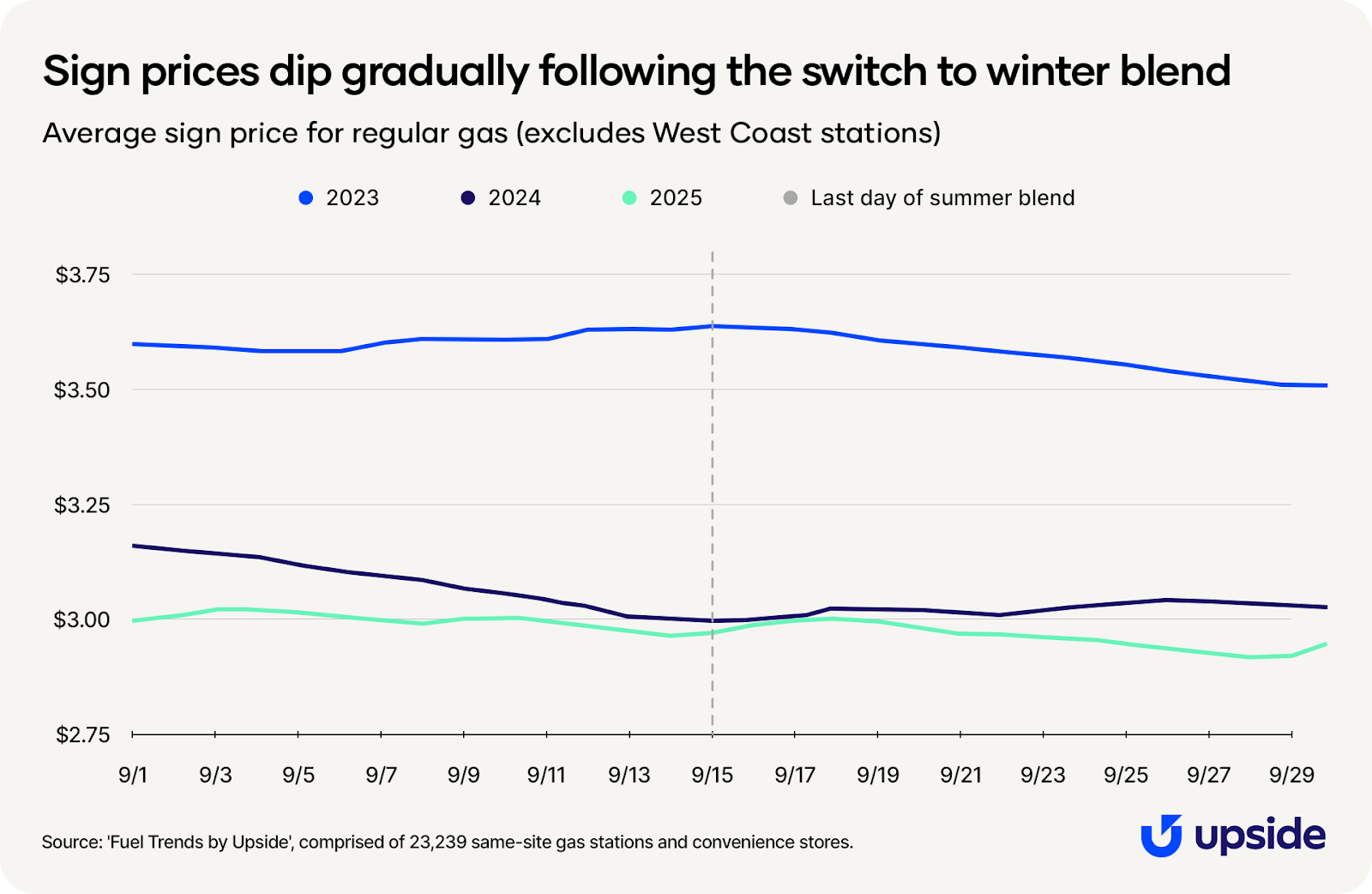

The chart below shows sign price changes during September from the past three years (excluding Western stations, which largely make the switch later, as noted). You can see that prices decline in the latter half of September as much of the country makes the switch.

Comparing the average prices from the first week of September to the last week, over the past three years, there are notable declines:

- 2023: -5.8 cents per gallon

- 2024: -10.2 cent per gallon

- 2025: -7.2 cents per gallon

The shift in pump prices doesn’t occur immediately — it slowly phases in over time. Just because stations can sell winter-blend fuel on September 16th doesn’t mean that they all do. First, most of them have to use up what remains of their summer blend inventory. And it’s not just stations that need to sell all of their summer blend fuel for the season — refineries need to do the same.

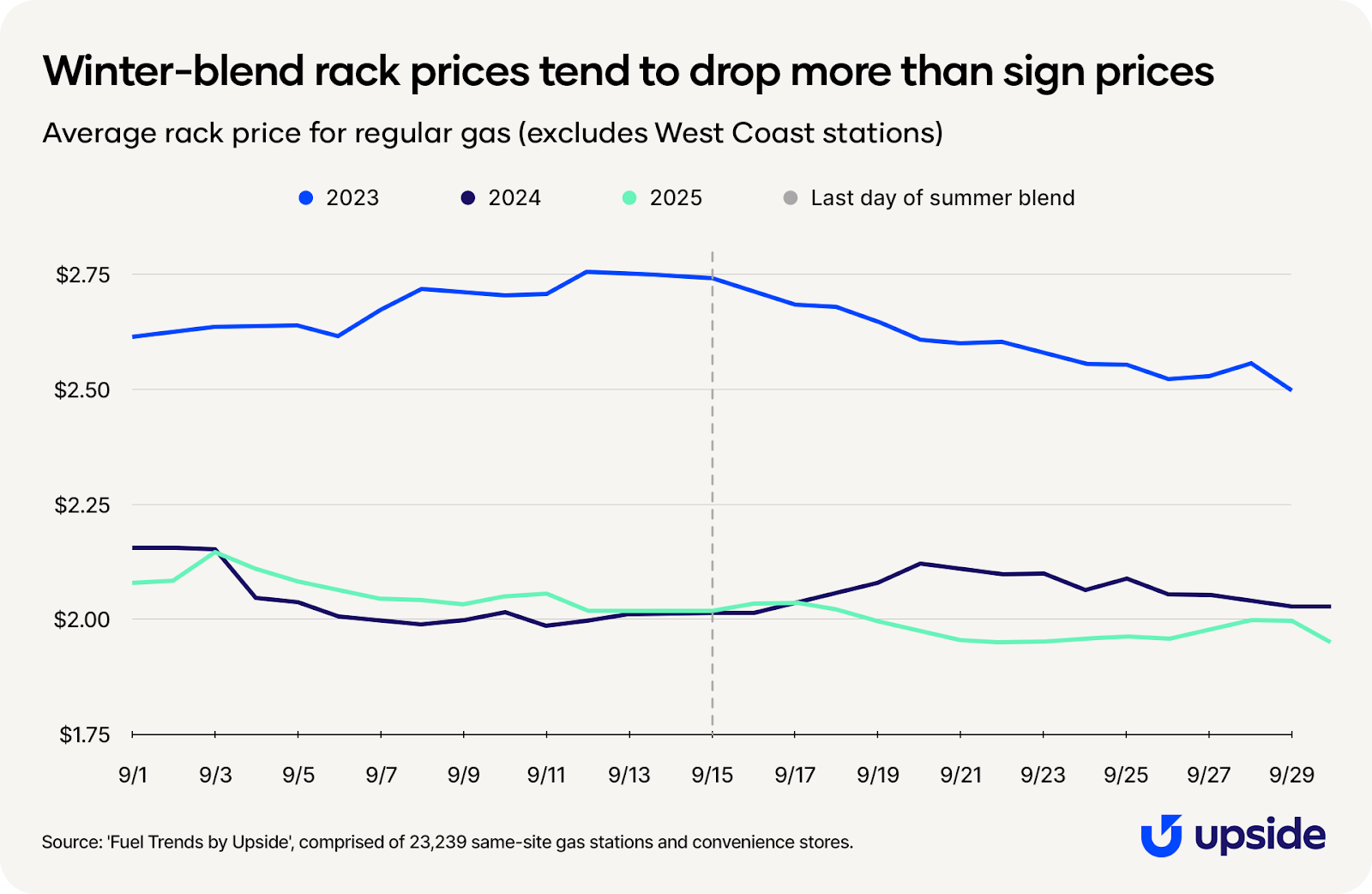

So now, let’s take a look at how rack prices change. Generally, we tend to see rack prices decline after the 15th — and to a faster degree than sign prices.

Here’s how the rack prices of the first week of September compared to the last week during each year:

- 2023: -10.0 cents per gallon

- 2024: -4.0 cents per gallon

- 2025: -12.0 cents per gallon

We can see that steeper declines aren’t automatic, however. In 2024, rack prices began increasing in the back half of the month, likely due to tightening supply ahead of Hurricane Helene. This goes to show how other macro factors can sometimes overpower the effect of the winter blend alone.

Predictions and considerations

Bracing for the slower winter season

The backslide in demand that started in September generally continues through October, as fewer drivers hit the roads during the colder months.

Some in the industry might be wondering about the impact of the ongoing federal government shutdown on transactions; to be sure, it could have a notable impact on demand in the Washington, D.C. region, where the largest share of furloughed government employees reside. Outside that region, we don’t expect anything more than a modest impact on demand, but the shutdown will simply tack on to otherwise slowing economic growth.

Here’s what else we have our eye on for October:

Potential tailwinds:

1. More stations will switch to winter-blend fuel, lowering sign prices in warmer regions like the West.

2. We’re seeing high oil output from both the United States and OPEC+, which is resulting in historically low prices.

Potential headwinds:

1. In the war between Russia and Ukraine, we’re seeing more frequent attacks on oil refineries. Further disruptions to the production of fuel in those regions could bring price increases.

2. Refinery maintenance increases in the fall, which will reduce supply in many areas.

3. Phillips 66 will stop production at its LA refinery in mid-October, further constraining supply to the Southern California market.

Want a closer look at the data?

Check out our insights hub with all our fuel and convenience monthly updates, plus special industry reports.

Share this article:

Dr. Thomas Weinandy

Dr. Weinandy is a Principal Research Economist at Upside, providing valuable insights into consumer spending behavior and macroeconomic trends for the fuel, grocery, and restaurant industries. With a Ph.D. in Applied Economics, his academic research is in digital economics and brick-and-mortar retail. He recently wrote a book on leveraging AI for business intelligence.

Similar articles

.png)

Request a demo

Request a demo of our platform with no obligation. Our team of industry experts will reach out to learn more about your unique business needs.